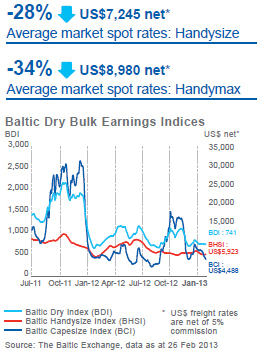

Excessive newbuilding deliveries in 2012 impacted freight rates across all dry bulk segments and drove the Baltic Dry Index (BDI) to its lowest annual average since 1987. Handysize and Handymax daily market spot rates averaged US$7,245 and US$8,980 in 2012 representing a year-on-year decline of 28% and 34% respectively. As in the previous year, the market for smaller bulk carriers declined less and demonstrated lower volatility than their larger, more expensive and less versatile siblings. Quite extraordinarily, Capesize and Panamax ships generated substantially the same average earnings as Handysize ships. Following a fourth quarter rally in 2011, dry bulk freight rates fell sharply to 26-year lows at the beginning of 2012 as a surge of newbuilding deliveries after the new year coincided with seasonal weather-related cargo disruptions and the Lunar New Year holidays in China. In the second and third quarters Handysize and Handymax rates benefited from more buoyant conditions while large bulk carrier earnings remained depressed. Small bulk carrier rates tapered off in the fourth quarter, whereas Capesize earnings rallied temporarily from a very low base on increased Chinese iron ore imports and a seasonal slowdown in new ship deliveries, only to collapse again in December to sub-Handysize levels. |

|

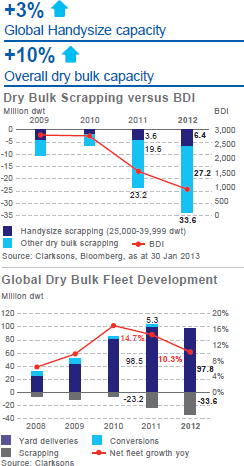

Newbuilding deliveries were only partly offset by scrapping, resulting in a significant 10% year-on-year net expansion of the dry bulk fleet. 98 million deadweight tonnes of new capacity delivered and a record 34 million tonnes - 5% of the existing fleet - was sold for scrap. It was this excessive net supply growth that undermined bulk carrier earnings overall in 2012. By contrast, the global fleet of 25,000-40,000 dwt Handysize ships in which we specialise expanded by only 3% net, benefitting from a significantly lower rate of deliveries, a high volume of scrapping and, overall, a more favourable global fleet age profile. A rapid influx of new ship deliveries gave way to markedly reduced deliveries in the fourth quarter, representing the first sign of slowing since the start of 2010. We are confident that the peak year for deliveries is now passed. Widespread slow-steaming reduced effective dry bulk shipping capacity in 2012. |

|

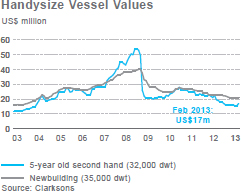

Clarksons' valuation of their benchmark five year old 32,000 dwt Handysize fell to US$15.5 million at the end of 2012 - a level not seen since before the dry bulk boom started in 2004 - and currently stands at US$17 million (down 13% from a year ago). |

|

|

Newbuilding prices are also now at pre-boom levels, having reduced 7% year on year to US$21 million due to competition among shipyards struggling to secure new contracts. |

|

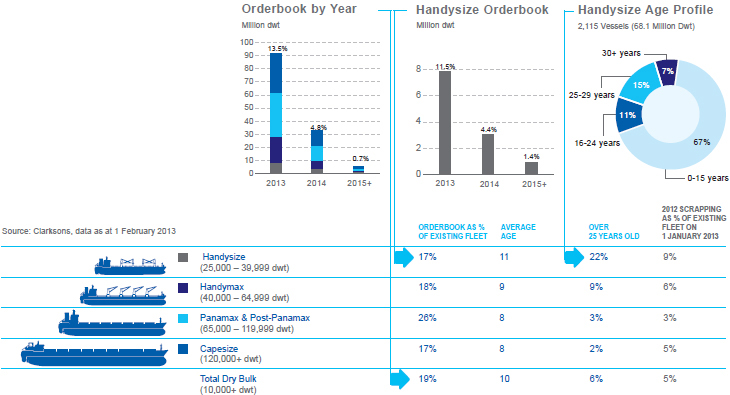

New bulk carrier ordering activity in 2012 decreased by 55% year on year, equivalent in capacity terms to 19% of actual newbuilding deliveries in 2012. This limited new ordering, combined with the heavy influx of new ship deliveries, has resulted in a significant reduction in the dry bulk orderbook from 30% a year ago to 19% today.

The Handysize orderbook now stands at 17% - down from 23% a year ago. The shipbuilding industry faces: i) shipyard capacity well in excess of requirements; ii) reduced access to bank funding curbing new ship ordering; iii) shipowners struggling with excessive borrowings; and iv) declining ship values and low freight rates.

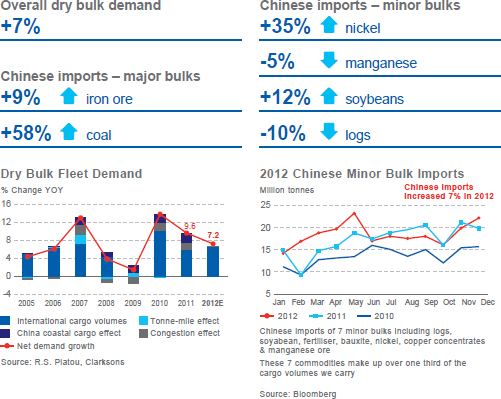

In the context of global economic uncertainty and low GDP growth, dry bulk transportation demand is estimated by R.S. Platou to have increased by a healthy 7% in 2012 year on year. Major bulk trade volumes expanded by over 5% with high-volume trade routes such as Chinese iron ore and coal imports setting new records. Chinese imports of seven important minor bulks increased 7% YOY in 2012 (see "Chinese Minor Bulk Imports" graph) thus lending strong support to global demand for Handysize and Handymax ships. However, the logs trade was impacted by a slowdown in the Chinese property sector. |

|