1 INTRODUCTION

1.1 General information

Pacific Basin Shipping Limited (the "Company") and its subsidiaries (together the "Group") are principally engaged in the provision of dry bulk shipping services internationally, and Towage services to the harbour and offshore sectors in Australia and New Zealand. In addition, the Group is engaged in the management and investment of the Group's cash and deposits through its treasury activities.

The Company was incorporated in Bermuda on 10 March 2004 as an exempted company with limited liability under the Companies Act 1981 of Bermuda.

The Company is listed on The Stock Exchange of Hong Kong Limited (the "Stock Exchange").

These financial statements have been approved for issue by the Board of Directors on 28 February 2013.

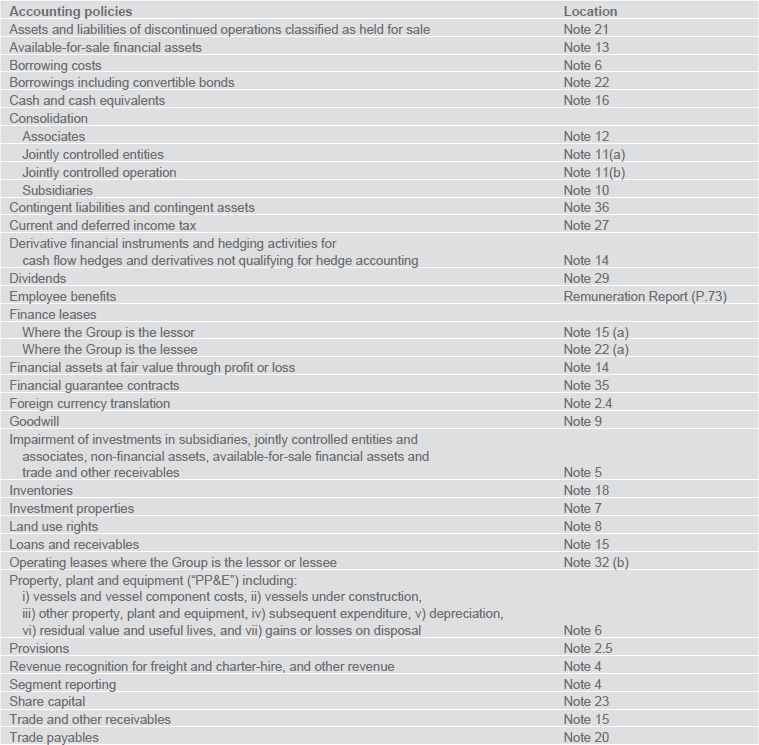

1.2 Presentation of the notes to the financial statements

The notes to the financial statements in this report are placed in order of significance to aid an understanding of the key drivers of the financial position of the Group, whilst maintaining the grouping of notes between income statement and balance sheet where appropriate.

Information relating to a specific financial statement line item has been brought together in one note. Hence:–

Principal Accounting Policies

are not shown separately but are included in the note or sections of this Annual Report for that item. They have been highlighted with this grey background. A navigation table is presented in Note 2.2.

| Critical Accounting Estimates and Judgements |

|---|

are not shown separately but are included in the note or sections of this Annual Report for that item. They have been highlighted with this white background with frame. A navigation table is presented in Note 3. |

Financial risk management has been integrated into the Risk Management Section. The auditable parts have been clearly marked and are listed below:

2 BASIS OF PREPARATION

2.1 Objective and accounting standards

The objective of these consolidated financial statements is to explain the results of the year ended 31 December 2012 and the financial position of the Group on that date, together with comparative information.

The financial statements have been prepared in accordance with Hong Kong Financial Reporting Standards ("HKFRS") issued by the Hong Kong Institute of Certified Public Accountants ("HKICPA"). The financial statements have been prepared under the historical cost convention, as modified by the revaluation of available-for-sale financial assets and financial assets and financial liabilities (including derivative instruments) at fair value through profit or loss, which are carried at fair value.

The preparation of financial statements in conformity with HKFRS requires the use of certain critical accounting estimates. It also requires management to exercise its judgement in the process of applying the Group's accounting policies. The areas involving a higher degree of judgement or complexity, or areas where assumptions and estimates are significant to these financial statements are listed under Note 3.

2.2 Accounting policies navigator

Except as described in Note 2.3, the Group's principal accounting policies have been consistently applied to each of the years presented in these financial statements. Certain comparative figures have been reclassified to conform to the current year's presentation.

2.3 Impact of new accounting policies

Certain new standards, amendments and improvements to standard are mandatory for the accounting period beginning 1 January 2012. However, the adoption of these new standards, amendments and improvements to standard does not result in any substantial change to the Group's accounting policies.

Certain new and amended standards, and improvements to HKFRS ("New Standards") are mandatory for accounting period beginning after 1 January 2012. The Group was not required to adopt these New Standards in the financial statements for the year ended 31 December 2012. Such New Standards that are relevant to the Group's operation are as follows:

The Group has already commenced an assessment of the impact of these New Standards but is not yet in a position to state whether they would have a significant impact on its results of operations and financial position.

2.4 Foreign currency translation

(a) Functional and presentation currency

The financial statements are presented in United States Dollars, which is the Company's functional and the Group's presentation currency. Items included in the financial statements of each of the Group's entities are measured using the currency of the primary economic environment in which the entity operates (the "functional currency"). Major business segments with non-US Dollar functional currencies include:

(i) PB Towage Segment: Australian Dollars, New Zealand Dollars and United States Dollars

(ii) The discontinued PB RoRo Segment: principally Euro

(b) Transactions and balances

Foreign currency transactions are translated into the functional currency at the exchange rates prevailing at the dates of the transactions. Foreign exchange gains and losses resulting from the settlement of such transactions and from the translation at year end exchange rates of monetary assets and liabilities denominated in foreign currencies are recognised in "general and administrative expenses" of the income statement, except when deferred in equity as qualifying cash flow hedges.

Translation difference on non-monetary financial assets and liabilities such as equities held at fair value through profit or loss are recognised in the income statement as part of the fair value gain or loss. Translation differences on non-monetary financial assets and liabilities such as equities classified as available-for-sale are included in the investment valuation reserve.

(c) Group companies

The results and financial position of each of the Group entities (none of which has the currency of a hyperinflationary economy) whose functional currency is different from the presentation currency is translated into the presentation currency as follows:

(i) assets and liabilities are translated at the closing rate on the balance sheet date;

(ii) income and expenses are translated at the average exchange rates (unless this average is not a reasonable approximation of the cumulative effect of the rates prevailing on the transaction dates, in which case income and expenses are translated at the dates of the transactions); and

(iii) all resulting exchange differences are recognised as a separate component of other comprehensive income.

Goodwill and fair value adjustments arising from the acquisition of a foreign entity are treated as assets and liabilities of the foreign entity and translated at the closing rate. Exchange differences arising are recognised in other comprehensive income.

When a foreign operation is partially or totally disposed of, exchange differences that were recorded in equity are reclassified to the consolidated income statement.

2.5 Provisions

Provisions are recognised when the Group has a present legal or constructive obligation as a result of past events; it is probable that an outflow of resources will be required to settle the obligation; and a reliable estimate of the amount can be made. Provisions are not recognised for future operating losses.

Where there are a number of similar obligations, the likelihood that an outflow will be required in settlement is determined by considering the class of obligations as a whole. A provision is recognised even if the likelihood of an outflow with respect to any one item included in the same class of obligations may be small.

Provisions are measured at the present value of the expenditures expected to be required to settle the obligation using a pre-tax rate that reflects current market assessments of the time value of money and the risks specific to the obligation. The increase in the provision due to the passage of time is recognised as interest expense.

3 CRITICAL ACCOUNTING ESTIMATES AND JUDGEMENTS

Estimates and judgements are continually evaluated and are based on historical experience and other factors, including expectations of future events that are believed to be reasonable under the circumstances.

The Group makes estimates and assumptions concerning the future. The resulting accounting estimates will, by definition, seldom equal the related actual results. The estimates and assumptions that carry a significant risk of causing a material adjustment to the carrying amounts of assets and liabilities within the next year are listed below with references to the locations of these items in the notes to the financial statements.

| Critical Accounting Estimates and Judgements | Location |

|---|---|

|

(a) Residual values of property, plant and equipment (b) Useful lives of vessels and vessel component costs (c) Impairment of vessels and vessels under construction (d) Classification of leases (e) Income taxes |

Note 6 Note 6 Note 6 Note 15(a) & 32(b) Note 27 |

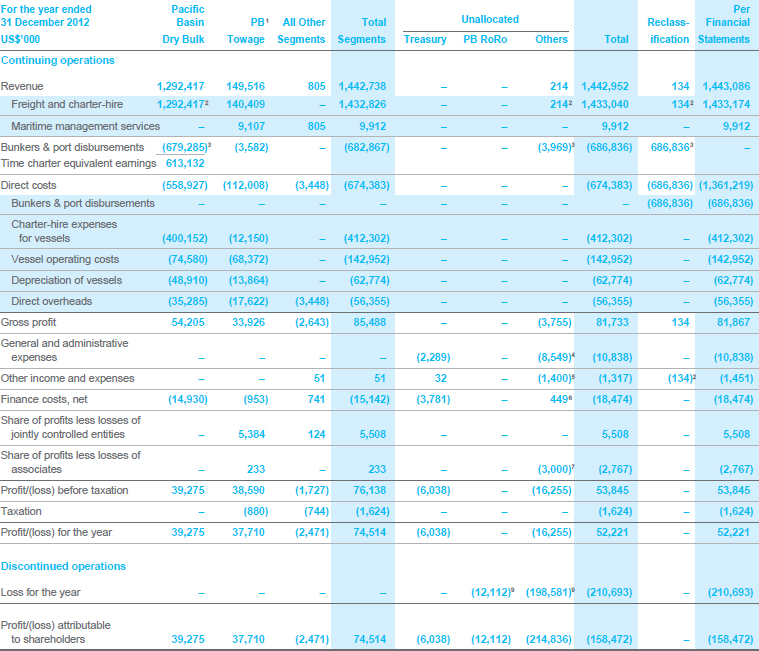

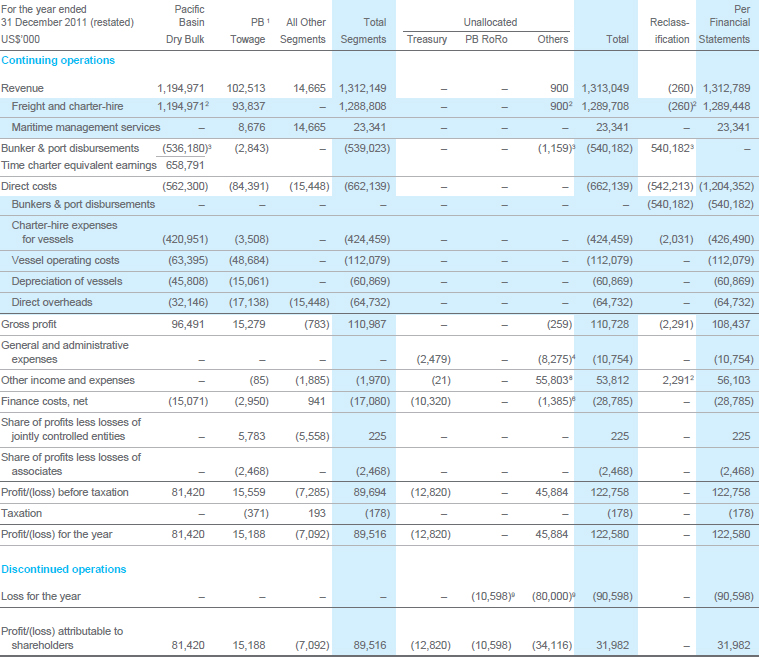

4 SEGMENT INFORMATION

The Group manages its businesses by divisions. Reports are presented to the heads of divisions as well as the Board for the purpose of making strategic decisions, allocation of resources and assessing performance. The reportable operating segments in this note are consistent with how information is presented to the heads of divisions and the Board.

The Group's revenue is primarily derived from the provision of dry bulk shipping services internationally, and Towage services to the harbour and offshore sectors in Australia and New Zealand.

The results of the port projects and maritime services activities are included in the "All Other Segments" column as they do not meet the quantitative thresholds suggested by HKFRS.

"Treasury" manages the Group's cash and borrowings. As such, related finance income and expenses are allocated under "Treasury".

Geographical segment information is not presented as the Directors consider that the nature of the provision of shipping services, which are carried out internationally, preclude a meaningful allocation of operating profit to specific geographical segments.

Accounting policy – Segment reporting

Management's approach to internal review and reporting to the heads of divisions and the Board is used as the basis for preparing segment information of the Group's material operating segments.

Accounting policy – Revenue recognition

Revenue comprises the fair value of the consideration for the sale of goods and services in the ordinary course of the Group's activities. Revenue is shown net of returns, rebates and discounts and after eliminating sales within the Group.

(i) Freight and charter-hire

The Group generates revenue from shipping activities, the principal sources of which are derived from the pools of Handysize and Handymax vessels.

Revenues from the pools of Handysize and Handymax vessels are derived from a combination of time charters and voyage charters. Revenue from a time charter is recognised on a straight-line basis over the period of the lease. Revenue from a voyage charter is recognised on a percentage-of-completion basis, which is determined on a time proportion method of the voyage.

(ii) Other revenue

Maritime management services income is recognised when the services are rendered.

Interest income is recognised on a time-proportion basis using the effective interest method.

Finance lease interest income is recognised over the term of the lease using the net investment method, based on a constant periodic rate of return.

Dividend income is recognised when the right to receive payment is established.

(a) Income statement segment information

(1) PB Towage, formerly known as PB Energy & Infrastructure Services, was renamed following the sale of PacMarine and closure of FBSL. Results of PacMarine and FBSL are under "All Other Segments".

(2) Net unrealised forward freight agreement benefits and expenses are under "Unallocated Others". Net realised benefits and expenses are under "Pacific Basin Dry Bulk". For the presentation of the financial statements, realised and unrealised benefits and expenses are reclassified to other income and other expenses. The related derivative assets and liabilities are also under "Unallocated Others".

(3) Net unrealised bunker swap contract benefits and expenses are under "Unallocated Others". Net realised benefits and expenses are under "Pacific Basin Dry Bulk". For the presentation of the financial statements, bunkers & port disbursements are reclassified to direct costs. The related derivative assets and liabilities are also under "Unallocated Others".

(4) Represents corporate overheads.

(5) Represents the impairment charge of US$1.4 million on unlisted equity securities.

(6) Represents net unrealised interest rate swap contract benefits and expenses.

(8) Represents gains on disposal of investment of US$55.8 million in Green Dragon Gas Limited in 2011.

(9) Comparatives are restated due to the discontinued RoRo operations classified as held for sale. The amount under "Unallocated Others" represents an impairment charge of US$190.4 million (2011: US$80.0 million) and an exchange loss arising from the disposal amounting to US$8.2 million (2011: Nil). Please see Note 21 for details.

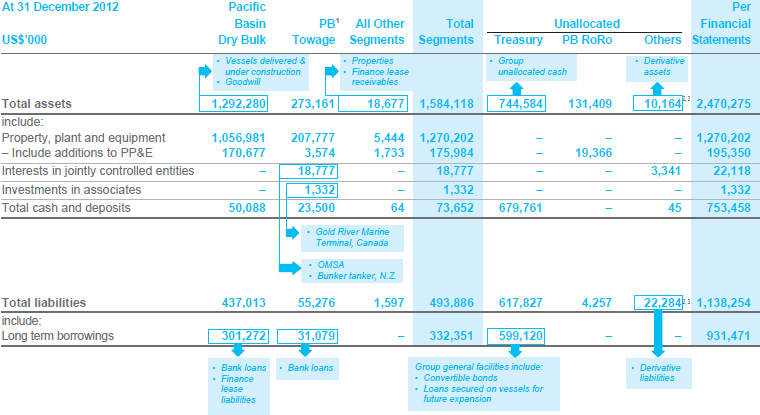

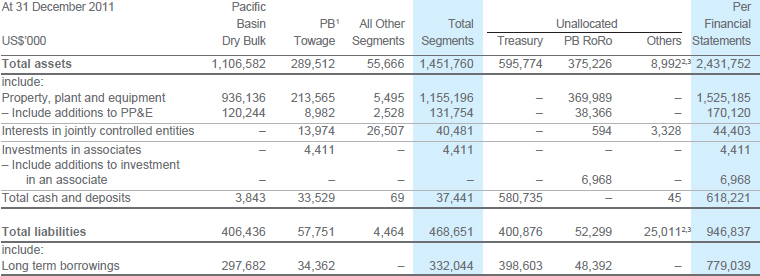

(b) Balance sheet segment information

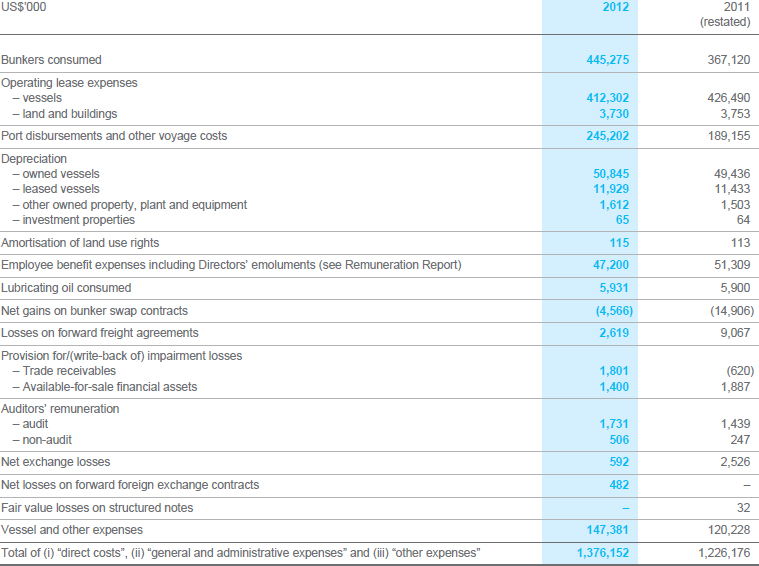

5 EXPENSES BY NATURE

General and administrative expenses

The Group incurred total administrative expenses of US$68.1 million (2011: US$77.2 million). Total administrative expenses comprised i) direct overheads of US$57.3 million (2011: US$66.4 million) including US$0.9 million (2011: US$1.8 million) for discontinued operations and ii) general and administrative expenses of US$10.8 million (2011: US$10.8 million). The decrease of US$9.1 million in direct overheads was primarily due to the sale of PacMarine business.

Depreciation

Owned vessels depreciation of US$50.8 million (2011: US$49.4 million) excludes an amount of US$7.9 million (2011: US$11.0 million) in relation to the RoRo vessels as this has been reclassified as part of the loss for the year on discontinued operations.

Other expenses

Movements in the fair value and payments for forward freight agreements amounted to US$2.6 million (2011: US$9.0 million). Taking into account the movements in fair value and receipts of US$2.5 million (2011: US$9.3 million) included in other income, the net movement in the fair value and payments for forward freight agreements resulted in an expense of US$0.1 million (2011: income of US$0.3 million).

Accounting policy – Impairment

Impairment of investments and non-financial assets

Assets that have an indefinite useful life, such as goodwill, are not subject to amortisation but are tested annually for impairment. Other assets are reviewed for impairment whenever events or changes in circumstances indicate that the carrying amount may not be recoverable. In assessing whether there is any indication that an asset may be impaired, internal and external sources of information are considered. If any such indication exists, the recoverable amount of the asset is assessed. An impairment loss is recognised for the amount by which the asset's carrying amount exceeds its recoverable amount, being the higher of (i) an asset's fair value less costs to sell and (ii) the value-inuse.

The fair value of vessels and vessels under construction is determined either by the market valuation or by independent valuers.

The value-in-use of the vessels represents estimated future cash flows from the continuing use of the vessels. For the purposes of assessing impairment, assets are grouped in the lowest levels at which there are separately identifiable cash flows. This level is described as a cash-generating unit ("CGU"). The way in which assets are grouped to form a CGU and the related cash flows associated with the CGU may in certain circumstances affect whether an impairment loss is recorded. Generally, the larger the grouping of assets and the broader the grouping of independent cash flows, the less likely it is that an impairment loss will be recorded as reductions in one cash inflow are more likely to be compensated by increases in other cash inflows within the same CGU.

Assets other than goodwill that suffered impairment are reviewed for possible reversal of the impairment at each balance sheet date.

Impairment of available-for-sale financial assets

The Group assesses at each balance sheet date whether there is objective evidence that a financial asset, or a group of financial assets, is impaired. In the case of equity security classified as available-for-sale, a significant or prolonged decline in the fair value of the security below its cost is considered as an indicator that the securities are impaired. If any such evidence exists, the cumulative loss – measured as the difference between the acquisition cost and the current fair value, less any impairment loss on that financial asset previously recognised in the income statement – is removed from equity and recognised in the consolidated income statement. Impairment losses recognised in the consolidated income statement on equity securities are not reversed through the consolidated income statement.

Impairment of trade and other receivables

A provision for impairment of trade and other receivables is established when there is objective evidence that the Group will not be able to collect the amount due according to the original terms of that receivable. Significant financial difficulties of the debtor, probability that the debtor will enter bankruptcy or financial reorganisation, and default or delinquency in payments are considered indicators that the trade receivable is impaired. The amount of the provision is the difference between the asset's carrying amount and the present value of estimated future cash flows, discounted at the original effective interest rate. The carrying amount of the assets is reduced through the use of an allowance account, and the amount of the loss is recognised in the income statement within "direct costs". When a trade receivable is uncollectable, it is written off against the provision for impairment.

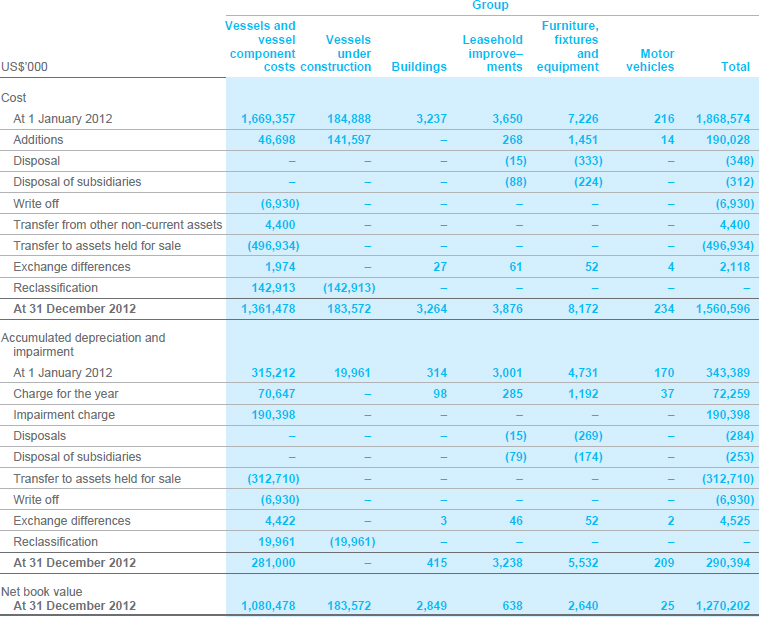

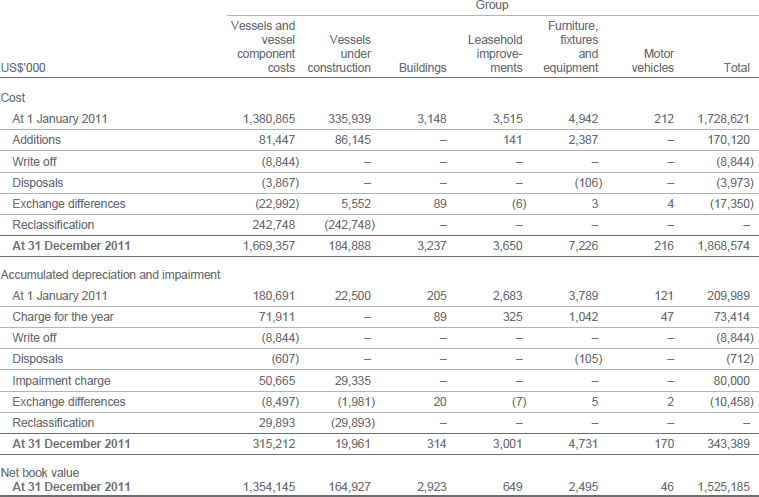

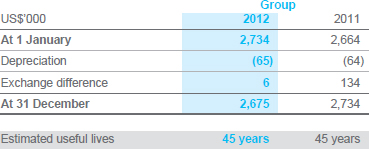

6 PROPERTY, PLANT AND EQUIPMENT

Estimated useful lives for towage vessels changed from 25 years to 30 years effective from 1 July 2011. The change in useful lives decreased the depreciation charge for 2012 by US$2,478,000 (2011: US$1,336,000).

As at 31 December 2012:

(a) Vessels and vessel component costs

(b) Certain owned vessels of net book value of US$695,556,000 (2011: US$548,532,000) were pledged to banks as securities for bank loans granted to certain subsidiaries of the Group (Note 22(b)(i)).

(c) Vessels under construction includes an amount of US$2,949,000 (2011: US$73,778,000) paid by the Group in relation to vessels whose construction work had not yet commenced.

(d) During the year, the Group had capitalised borrowing costs amounting to US$3,642,000 (2011: US$1,280,000) on qualifying assets. Borrowing costs were capitalised at the weighted average rate of 3.2% of the Group's unhedged borrowings not allocated to the two business segments (Note 26).

Accounting policies – Property, plant and equipment

Please refer to Note 5 for the accounting policy on impairment and Note 22(a) for that on finance leased fixed assets.

Vessels and vessel component costs

Vessels are stated at cost less accumulated depreciation and accumulated impairment losses. The cost of an asset comprises its purchase price and any directly attributable cost of bringing the asset to its working condition for its intended use. Cost may also include transfers from equity of any gains/losses on qualifying cash flow hedges of foreign currency purchases of vessels.

Vessel component costs include the cost of major components which are usually replaced or renewed at drydockings. The assets are stated at cost less accumulated depreciation and accumulated impairment losses. The Group subsequently capitalises drydocking costs as they are incurred.

Vessels under construction

Vessels under construction are stated at cost and are not subject to depreciation. All direct costs relating to the construction of vessels, including borrowing costs (see below) during the construction period, are capitalised as cost of vessels. When the assets concerned are brought into use, the costs are transferred to vessels and vessel component costs and depreciated in accordance with the policy on depreciation.

Borrowing costs

Borrowing costs incurred for the construction of any qualifying asset are capitalised during the period of time that is required to complete and prepare the asset for its intended use. Other borrowing costs are expensed.

Other property, plant and equipment

Other property, plant and equipment, comprising buildings, leasehold improvements, furniture, fixtures and equipment and motor vehicles, are stated at cost less accumulated depreciation and accumulated impairment losses.

Subsequent expenditure

Subsequent expenditure is either included in the carrying amount of the assets or recognised as a separate asset, as appropriate, only when it is probable that future economic benefits associated with the expenditure will accrue to the Group and such expenditure can be measured reliably. The carrying amount of a replaced part is written off. All other repairs and maintenance are expensed in the income statement during the financial period in which they are incurred.

Depreciation

Depreciation of property, plant and equipment is calculated using straight-line method to allocate their cost to their residual values over their remaining estimated useful lives.

Residual values and useful lives

The residual values of the Group's assets are defined as the estimated amounts that the Group would currently obtain from disposal of the assets, after deducting the estimated costs of disposals, as if the assets were already of the age and in the conditions expected at the end of their useful lives.

Useful lives of the Group's vessels and vessel component costs are defined as the period over which they are expected to be available for use by the Group.

The assets' residual values and useful lives are reviewed, and adjusted if appropriate, at each balance sheet date.

Gains or losses on disposal

Gains or losses on disposal are determined by comparing the proceeds with the carrying amounts and are recognised in the income statement.

| Critical accounting estimates and judgements – |

|---|

|

Residual values of property, plant and equipment The Group estimates residual values of its vessels by reference to the lightweight tonnes of the vessels and the average demolition steel price of similar vessels in the Far East market and Indian Sub-Continent market.

With all other variables held constant, if the residual value increases/decreases by 10% from management estimates, the depreciation expense would decrease/increase by US$0.8 million in the next year. Useful lives of vessels and vessel component costs The Group estimates useful life of its vessels by reference to the average historical useful life of similar class of vessels, their expected usage, expected repair and maintenance programme, and technical or commercial obsolescence arising from changes or improvements in the vessel market. The Group estimates the useful life of its vessel component costs by reference to the average historical periods between drydocking cycles of vessels of similar age, and the expected usage of the vessel until its next drydock.

With all other variables held constant, if the useful lives increase/decrease by 3 years from management estimates, the depreciation expense would decrease by US$9.3 million or increase by US$13.6 million in the next year. Impairment of vessels and vessels under construction The Group tests whether the carrying value of vessels and vessels under construction have suffered any impairment in accordance with the accounting policy on impairment of investments and non-financial assets (note 5). In assessing the fair market value and value-in-use, the Group reviews indicators of potential impairment such as reported sale and purchase prices, market demand and general market conditions as well as market valuations from leading, independent and internationally recognised shipbroking companies. The value-in-use of the vessels is an assessment of assumptions and estimates of vessel future earnings and appropriate discount rates to derive the present value of those earnings. The discount rates used are based on the industry sector risk premium relevant to the CGU and the applicable gearing ratio of the CGU. The applicable discount rates applied for future cash flows in each segment for 2012 are as follow:

i) Pacific Basin Dry Bulk: 7.9% (2011: 8.7%)

With all other variables held constant, increasing the discount rates of Pacific Basin Dry Bulk or PB Towage by 1% from the original estimate will not give rise to any impairment. |

7 INVESTMENT PROPERTIES

The investment properties were valued at 31 December 2012 by an independent qualified valuer on the basis of market value. The fair value of the investment properties was approximately US$4,192,000 (2011: US$4,092,000).

Accounting policy

Investment properties comprising mainly buildings are held for a combination of rental yields and capital appreciation. Investment properties are stated initially at cost and subsequently carried at cost less accumulated depreciation and accumulated impairment losses. Depreciation is calculated using a straight-line method to allocate their costs to their residual values over their estimated useful lives. The residual values and useful lives of investment properties are reviewed, and adjusted if appropriate, at each balance sheet date.

Please refer to Note 5 for the accounting policy on impairment.

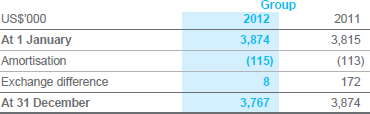

8 LAND USE RIGHTS

The Group's interest in land use rights represents prepaid operating lease payments in the PRC with lease periods between 10 to 50 years. The land use rights related to "Buildings" in Note 6 & "Investment Properties" in Note 7.

Accounting policy

The upfront prepayments made for land use rights are expensed in the income statement on a straight line basis over the period of the lease or, when there is impairment, are recognised in the income statement immediately.

Please refer to Note 5 for the accounting policy on impairment.

9 GOODWILL

Goodwill represents the excess of the cost of acquisition over the fair value of the Group's share of the net identifiable assets of the acquired subsidiary at the date of acquisition.

The recoverable amount of Pacific Basin Dry Bulk to which the goodwill relates has been determined based on a value-in-use calculation over its useful life. The calculation is based on a one-year budget and a further two-year outlook. Key assumptions were based on past performance, management's expectations on market development and general inflation. Cash flows beyond the three year period are extrapolated assuming zero growth and no material change in the existing scope of business, business environment and market conditions. The discount rate applied to the cash flow projections is 7.9% (2011: 8.7%) reflecting the Group's cost of capital.

Based on the assessment performed, no impairment provision against the carrying value of goodwill is considered necessary.

Accounting policy

Goodwill is carried at cost less accumulated impairment losses. Gains and losses on the disposal of an entity include the carrying amount of goodwill relating to the entity being sold. It is tested annually for impairment in accordance with the accounting policy on impairment in Note 5. Impairment losses on goodwill are not reversible.

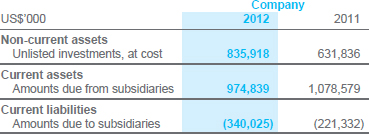

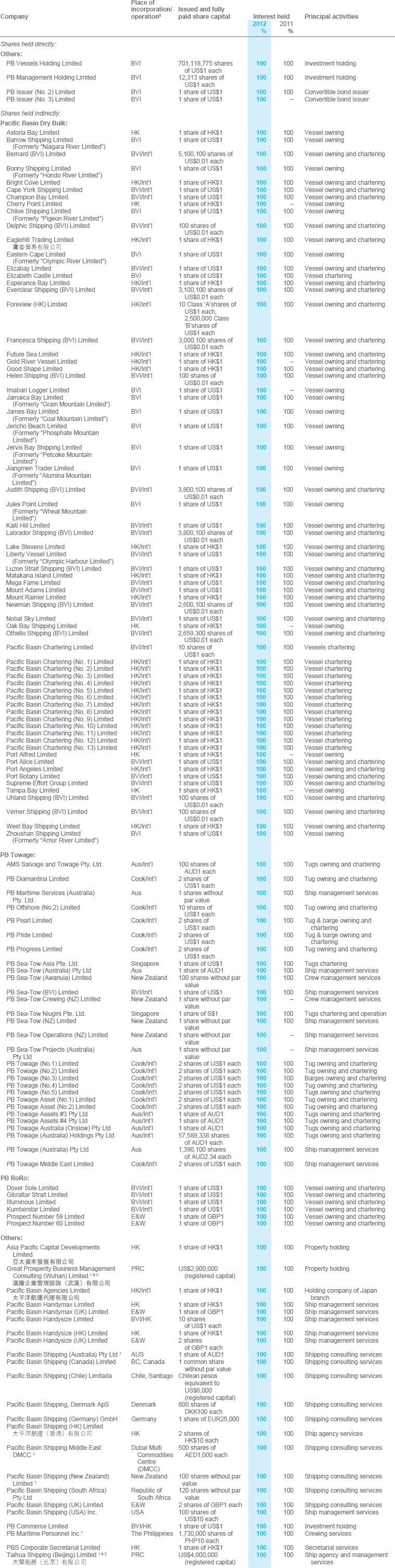

10 SUBSIDIARIES

The amounts due from and to subsidiaries are unsecured, non-interest bearing and repayable on demand.

The carrying values of amounts due from and to subsidiaries approximate their fair values due to the short-term maturities of these assets and liabilities.

Details of principal subsidiaries of the Group as at 31 December 2012 are set out in Note 38.

Accounting policy – Consolidation

Subsidiaries are all entities (including special purpose entities) over which the Group has the power to govern the financial and operating policies generally accompanying a shareholding of more than one half of the voting rights.

The existence and effect of potential voting rights that are currently exercisable or convertible are considered when assessing whether the Group controls another entity.

Subsidiaries are fully consolidated from the date on which control is transferred to the Group. They are deconsolidated from the date that control ceases.

The Group uses the acquisition method to account for business combinations. The consideration transferred for the acquisition of a subsidiary is the fair value of the assets transferred, the liabilities incurred and the equity interests issued by the Group. The consideration transferred includes the fair value of any asset or liability resulting from a contingent consideration arrangement. Acquisition-related costs are expensed as incurred. Identifiable assets and liabilities and contingent liabilities assumed in a business combination are measured initially at their fair values at the acquisition date.

The excess of the consideration transferred, the amount of any non-controlling interest in the acquiree and the acquisition-date fair value of any previous equity interest in the acquiree over the fair value of the identifiable net assets acquired is recorded as goodwill. If this is less than the fair value of the net assets of the subsidiary acquired, the difference is recognised directly in the income statement. In each acquisition case, the Group recognises any non-controlling interest in the acquiree either at fair value or at the non-controlling interest's proportionate share of the acquiree's net assets.

Intercompany transactions, balances and unrealised gains on transactions between group companies are eliminated. Unrealised losses are also eliminated unless the transaction provides evidence of an impairment of the asset transferred. The financial information of subsidiaries has been changed where necessary to ensure consistency with the policies adopted by the Group.

In the Company's balance sheet, the investments in subsidiaries are stated at cost less provision for impairment losses. Cost is adjusted to reflect changes in consideration arising from contingent consideration amendments. Cost also includes direct attributable costs of investments. The results of subsidiaries are accounted for by the Company on the basis of dividends received and receivable.

Please refer to Note 5 for the accounting policy on impairment.

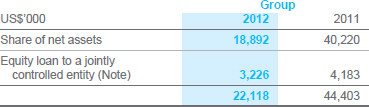

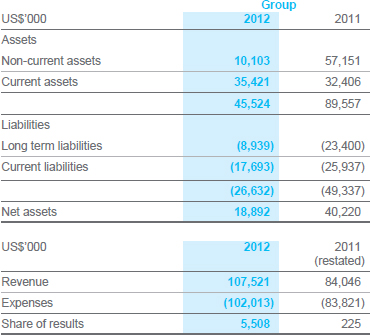

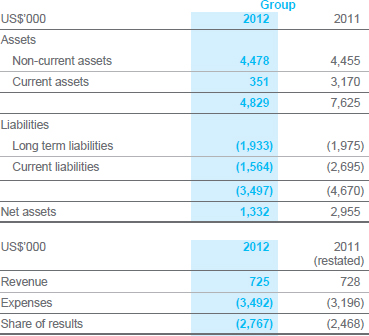

11 INTERESTS IN JOINT VENTURES

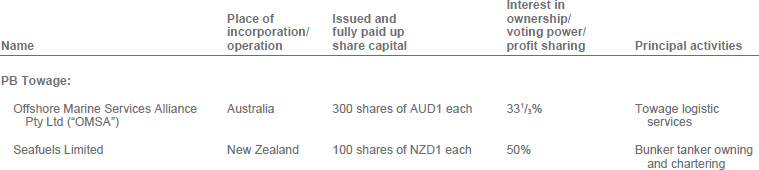

(a) Jointly controlled entities

Note: The equity loan to Seafuels Limited is unsecured, non-interest bearing, and has no fixed repayment terms and the Group does not intend to request for repayment within twelve months.

An analysis of the Group's effective share of assets, liabilities, revenue and expenses of the jointly controlled entities is set out below:

There are no contingent liabilities relating to the Group's interests in jointly controlled entities, and there are no contingent liabilities or commitments of the jointly controlled entities themselves.

The Nanjing cargo terminal was disposed of in 2012.

Accounting policy – Jointly controlled entities

A jointly controlled entity is a contractual arrangement whereby the Group and other parties undertake an economic activity which is subject to joint control and none of the participating parties has unilateral control over the economic activity.

Interests in jointly controlled entities are accounted for in the consolidated financial statements using the equity method of accounting and are initially recognised at cost. The Group's interests in jointly controlled entities include goodwill (net of any accumulated impairment losses) identified on acquisition.

The Group's share of its jointly controlled entities' post-acquisition profits or losses is recognised in the consolidated income statement and its share of post-acquisition reserves is recognised in other comprehensive income based on the relevant profit sharing ratios.

The Group recognises the portion of gains or losses on the sale of assets by the Group to the jointly controlled entity that it is attributable to the other venturers. The Group does not recognise its share of profits or losses from the jointly controlled entity that results from the purchase of assets by the Group from the jointly controlled entity until it resells the assets to an independent party. However, a loss on the transaction is recognised immediately if the loss provides evidence of a reduction in the net realisable value of current assets, or an impairment loss. The financial information of jointly controlled entities has been adjusted where necessary to ensure consistency with the policies adopted by the Group.

Please refer to Note 5 for the accounting policy on impairment.

Details of the principal jointly controlled entities of the Group held indirectly by the Company at 31 December 2012 are as follows:

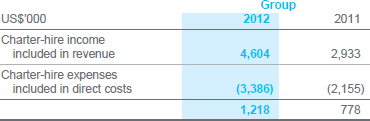

(b) Jointly controlled operation

In 2012, the Group had a contractual arrangement with a third party to share equally the operating result associated with the chartering of a vessel (jointly controlled operation). The amounts of income and expenses recognised in respect of the Group's interest in the jointly controlled operation are as follow:

Accounting policy – Jointly controlled operation

A jointly controlled operation is a contractual arrangement whereby the Group and other parties combine their operations, resources and expertise to undertake an economic activity in which each party takes a share of the revenue and costs in the economic activity, such a share being determined in accordance with the contractual arrangement.

The assets that the Group controls and liabilities that the Group incurs in relation to the jointly controlled operation are recognised in the consolidated balance sheet on an accrual basis and classified according to the nature of the item. The expenses that the Group incurs and its share of income that it earns from the jointly controlled operations are included in the consolidated income statement.

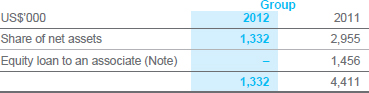

12 INVESTMENTS IN ASSOCIATES

Note: The equity loan to an associate, Muchalat Industries Limited, was unsecured, non-interest bearing, and had no fixed repayment terms.

An analysis of the Group's effective share of assets, liabilities, revenue and expenses of the associates is set out below:

Accounting policy – Associates

An associate is an entity over which the Group has significant influence but no control, generally accompanying a shareholding of between 20% and 50% of the voting rights.

Investments in associates are accounted for in the consolidated financial statements using the equity method of accounting and are initially recognised at cost. The Group's investments in associates include goodwill (net of any accumulated impairment losses) identified on acquisition.

The Group's share of its associates' post-acquisition profits or losses is recognised in the consolidated income statement, and its share of post-acquisition movements in reserves is recognised in other comprehensive income based on the relevant profit sharing ratios. The cumulative post-acquisition movements are adjusted against the carrying amount of the investment. When the Group's share of losses in an associate equals or exceeds its interest in the associate, including any other unsecured receivables, the Group does not recognise further losses, unless it has incurred obligations or made payments on behalf of the associate.

Unrealised gains on transactions between the Group and its associates are eliminated to the extent of the Group's interest in the associates. Unrealised losses are also eliminated unless the transaction provides evidence of an impairment of the asset transferred. The financial information of the associates has been changed where necessary to ensure consistency with the policies adopted by the Group.

Please refer to Note 5 for the accounting policy on impairment.

Details of the principal associate of the Group held indirectly by the Company at 31 December 2012 are as follows:

13 AVAILABLE-FOR-SALE FINANCIAL ASSETS

Available-for-sale financial assets are denominated in United States Dollars.

(a) This represents the Group's investment in Greka Drilling Limited, a company listed on the London AIM market.

(b) This represents the Group's investment in an unlisted renewable energy equity fund.

Available-for-sale financial assets have been analysed by valuation method as above and the levels are defined as follows:

Fair value levels

- Level 1: Quoted prices (unadjusted) in active markets for identical assets or liabilities.

- Level 2: Inputs other than quoted prices included within level 1 that are observable for the asset or liability, either directly (that is, as prices) or indirectly (that is, derived from prices).

- Level 3: Inputs for the asset or liability that are not based on observable market data (that is, unobservable inputs).

Changes in Level 3 financial instruments, unlisted equity securities, for the year ended 31 December 2012 are as follows:

Accounting policy – Available-for-sale financial assets

Available-for-sale financial assets are non-derivatives that are either designated in this category or not classified in any other categories under financial assets. They are included in non-current assets unless management intends to dispose of them within twelve months from the balance sheet date.

Assets in this category are initially recognised at fair value plus transaction costs and are subsequently carried at fair value. Gains and losses arising from changes in the fair value are recognised in other comprehensive income.

When securities classified as available-for-sale are sold or impaired, the accumulated fair value adjustments recognised in equity are released to the income statement.

Interest on available-for-sale securities calculated using the effective interest method is recognised in the income statement as part of finance income. Dividends on available-for-sale equity instruments are recognised in the income statement as part of other income when the Group's right to receive payments is established.

The fair values of quoted investments are based on current bid prices. If the market for a financial asset is not active (and for unlisted securities), the Group establishes fair value by using appropriate valuation techniques. These include the use of recent arm's length transactions, reference to other substantially similar instruments, and discounted cash flow analysis.

Please refer to Note 5 for the accounting policy on impairment.

14 DERIVATIVE ASSETS AND LIABILITIES

Derivative assets and liabilities have been analysed by valuation method. Please refer to Note 13 Fair value levels for the definitions of different levels.

The Group is exposed to fluctuations in freight rates, bunker prices, interest rates and currency exchange rates. The Group manages these exposures by way of:

- forward freight agreements ("FFA");

- bunker swap contracts;

- interest rate swap contracts; and

- forward foreign exchange contracts.

Amongst the derivative assets and liabilities held by the Group, the fair values of forward foreign exchange contracts, interest rate swap contracts and bunker swap contracts are quoted by dealers at the balance sheet date. The forward freight agreements are traded through a clearing house and its fair value is determined using forward freight rates at the balance sheet date. The rest of the derivative assets and liabilities are over-the-counter derivatives which are not traded in an active market.

(a) Forward foreign exchange contracts

(i) Forward foreign exchange contracts that qualify for hedge accounting as cash flow hedges

The Group has long term bank borrowings denominated in Danish Kroner ("DKK") with maturity in August 2023. To hedge against the potential fluctuations in foreign exchange, the Group entered into forward foreign exchange contracts with terms that match the repayment schedules of the long term bank borrowings. These forward foreign exchange contracts qualify for hedge accounting as cash flow hedges.

At 31 December 2012, the Group had outstanding forward foreign exchange contracts with banks to buy approximately DKK 1,442.7 million (2011: Nil) and simultaneously sell approximately US$260.8 million (2011: Nil), which expire through August 2023.

At 31 December 2011, the Group had outstanding forward foreign exchange contracts with banks to buy approximately DKK 615.8 million and simultaneously sell approximately EUR 82.7 million, which originally expired through February 2023. Such forward foreign exchange contracts were terminated in 2012.

At 31 December 2012, the Group had outstanding forward foreign exchange contracts with banks to buy approximately US$181.1 million (2011: Nil) and simultaneously sell approximately EUR 140.0 million (2011: Nil) for the sales proceeds of our six RoRo vessels that are denominated in Euros. These contracts expire through December 2015.

(ii) Forward foreign exchange contracts that do not qualify for hedge accounting

At 31 December 2012, the Group had outstanding forward foreign exchange contracts with banks to buy approximately US$79.6 million (2011: Nil) and simultaneously sell approximately EUR 60.7 million (2011: Nil) for our cash that are denominated in Euros. These contracts expire through July 2013.

- Sensitivity analysis:

With all other variables held constant, if the currencies of Non-Functional Currency Items had weakened/strengthened by 3% against United States Dollars, the Group's profit after tax and equity would have been decreased/increased by US$2.3 million (2011: US$2.7 million) mainly as a result of translation of cash and deposits denominated in Australian Dollars.

(b) Bunker swap contracts

The Group enters into bunker swap contracts to manage the fluctuations in bunker prices in connection with the Group's long-term cargo contract commitments.

At 31 December 2012, the Group had outstanding bunker swap contracts to buy approximately 201,150 (2011: 140,000) metric tonnes of bunkers. These contracts expire through December 2017 (2011: June 2016).

- Sensitivity analysis:

With all other variables held constant, if the average forward bunker rate on the bunker swap contracts held by the Group at the balance sheet date had been 10% higher/lower, the Group's profit after tax and equity would increase/decrease by approximately US$12.1 million (2011: US$8.3 million). Future movements in bunker price will be reflected in the eventual operating results derived from the vessels, which would offset such increase/decrease of the Group's profit after tax and equity.

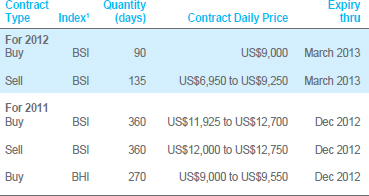

(c) Forward freight agreements

The Group enters into forward freight agreements as a method of managing its exposure to both its physical tonnage and cargo with regard to its Handysize and Handymax vessels.

At 31 December 2012, the Group had outstanding forward freight agreements as follows:

(1) "BSI" represents "Baltic Supramax Index" and "BHI" represents "Baltic Handysize Index".

- Sensitivity analysis:

With all other variables held constant, if the average forward freight rate on FFA contracts held by the Group at the balance sheet date had been 20% higher/lower, the Group's profit after tax and equity would decrease/increase by approximately US$0.1 million (2011: increase/decrease by US$0.5 million). Future movements in charter rates will be reflected in the eventual operating revenue derived from the vessels, which would offset such decrease/increase of the Group's profit after tax and equity.

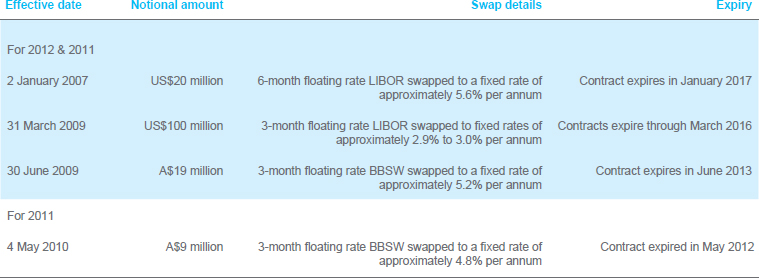

(d) Interest rate swap contracts

The Group has bank borrowings exposed to floating interest rates. In order to hedge against the fluctuations in interest rates related to the bank borrowings, the Group entered into interest rate swap contracts with banks to manage exposure to 3-month and 6-month floating rate LIBOR, and 3-month floating Bank Bill Swap Reference Rate ("BBSW").

(i) Interest rate swap contracts that qualify for hedge accounting as cash flow hedges

(ii) Interest rate swap contracts that do not qualify for hedge accounting

Effective from 2 January 2007, a notional amount of US$40 million with the 6-month floating rate LIBOR swapped to a fixed rate of approximately 5.0% per annum so long as the 6-month floating rate LIBOR remains below the agreed cap strike level of 6.0%. This fixed rate switches to a discounted floating rate (discount is approximately 1.0%) for the 6-month fixing period when the prevailing 6-month floating rate LIBOR is above 6.0% and reverts back to the fixed rate should the 6-month floating rate LIBOR subsequently drop below 6.0%.

This contract expires in January 2017.

- Sensitivity analysis:

With all other variables held constant, if the average interest rate on net cash balance subject to floating interest rates, which includes cash and deposits net of unhedged bank loans, held by the Group at the balance sheet date had been 50 basis point higher/lower, the Group's profit after tax and equity would increase/decrease by approximately US$3.4 million (2011: US$2.6 million).

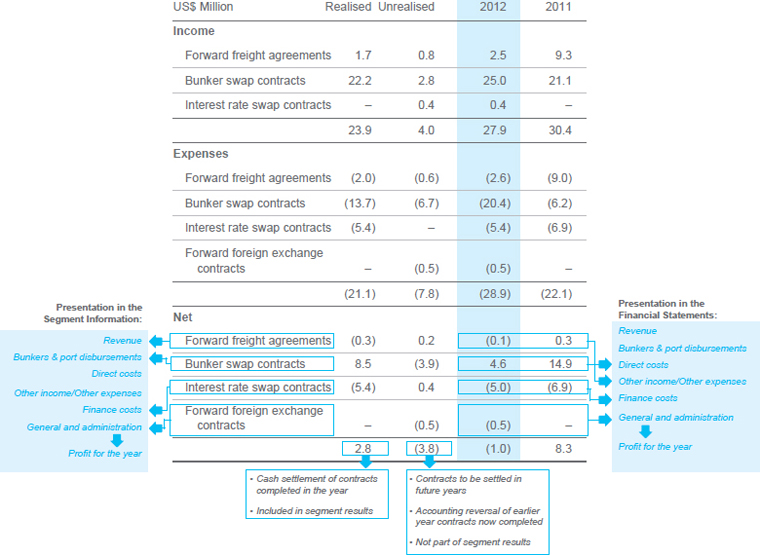

During the year ended 31 December 2012, the Group recognised net derivative expense of US$1.0 million, as follows:

The application of HKAS 39 "Financial Instruments: Recognition and Measurement" has the effect of shifting to this year the estimated results of these derivative contracts that expire in future periods. In 2012 this created a net unrealised non-cash expense of US$3.8 million (2011: US$1.6 million). The cash flows of these contracts will occur in future reporting years.

Accounting policy –

Financial assets at fair value through profit or loss

Financial assets at fair value through profit or loss are financial assets held for trading. A financial asset is classified in this category if acquired principally for the purpose of selling in the short term. Derivatives are classified as held for trading unless they are designated as hedges. Derivatives are classified as current and non-current assets according to their respective settlement dates.

Financial assets at fair value through profit or loss are initially recognised at fair value, and transaction costs are expensed in the income statement, and are subsequently remeasured at their fair values. Gains and losses arising from changes in the fair values are included in the other income or other expenses in the period in which they arise.

Dividend income from financial assets at fair value through profit or loss is recognised in the income statement as part of other income when the Group's right to receive payments is established.

In the cash flow statement, financial assets held for trading are presented within "operating activities" as part of changes in working capital.

Derivative financial instruments and hedging activities

The method of recognising the resulting gain or loss arising from changes in fair value for derivative financial instruments depends on whether the derivative is designated as a hedging instrument, and if so, the nature of the item being hedged. The Group designates certain derivatives as cash flow hedges.

The Group documents at the inception of the transaction the relationship between the hedging instruments and the hedged items, as well as its risk management objectives and strategy for undertaking various hedge transactions. The Group also documents its assessment, both at the hedge inception and on an ongoing basis, of whether the derivatives that are used in the hedging transactions are highly effective in offsetting the changes in fair values or cash flows of the hedged items.

The full fair value of a hedging derivative is classified as a non-current asset or liability when the remaining maturity of the hedged item is more than twelve months after the balance sheet date. A trading derivative is classified as a current asset or liability.

(i) Cash flow hedges

The effective portion of changes in the fair value of derivatives that are designated and qualify as cash flow hedges are recognised in other comprehensive income. The gain or loss relating to the ineffective portion is recognised immediately in the income statement within other income and expenses.

Amounts accumulated in equity are recycled in the income statement in the periods when the hedged item affects profit or loss. However, when the forecast transaction that is hedged results in the recognition of a non-financial asset or a liability, the gains and losses previously deferred in equity are transferred from equity and included in the initial measurement of the cost of the asset or liability. The deferred amounts are ultimately recognised in depreciation in the case of property, plant and equipment.

When a hedging instrument expires or is sold, or when a hedge no longer meets the criteria for hedge accounting, any cumulative gain or loss existing in equity at that time remains in equity and is recycled when the forecast transaction is ultimately recognised in the income statement. When a forecast transaction is no longer expected to occur, the cumulative gain or loss that was recorded in equity is immediately transferred to the income statement.

(ii) Derivatives not qualifying for hedge accounting

Derivative instruments that do not qualify for hedge accounting are accounted for as financial assets and liabilities at fair value through profit or loss. Changes in the fair value of these derivative instruments are recognised immediately in the income statement.

Bunker swap contracts and forward freight agreements do not qualify for hedge accounting mainly because the contract periods, which are in calendar months, do not coincide with the periods of the physical contracts. The terms of one of the interest rate swap contracts and three forward foreign exchange contracts also did not qualify for hedge accounting.

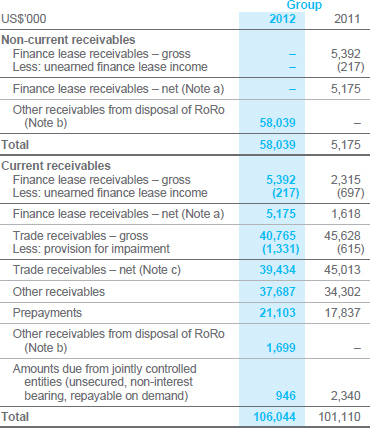

15 TRADE AND OTHER RECEIVABLES

The carrying values of trade and other receivables approximate their fair values due to their short-term maturities.

Trade and other receivables are mainly denominated in United States Dollars.

Accounting policy – Loan receivables, trade and other receivables

Loans and receivables are non-derivative financial assets with fixed or determinable payments that are not quoted in an active market. They are included in current assets, except for maturities greater than twelve months after the balance sheet date. These are classified as non-current assets. Trade and other receivables in the balance sheet are classified as loans and receivables.

Loans and receivables are recognised initially at fair value, plus transaction costs incurred. Loans and receivables are subsequently carried at amortised cost using the effective interest method.

Trade receivables mainly represent freight and charter-hire receivables which are recognised initially at fair value and subsequently measured at amortised cost using effective interest method, less provision for impairment.

Please refer to Note 5 for the accounting policy on impairment.

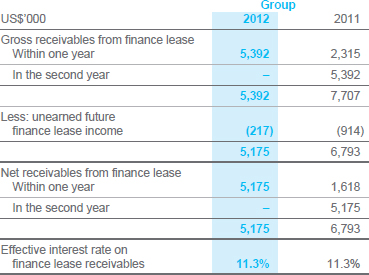

(a) Finance leases receivables

At 31 December 2012, one of the Group's vessels was leased out under a finance lease. Under the terms of the lease, the charterer has the obligation to purchase the vessel at the end of the lease period.

The gross receivables, unearned finance lease income and the net receivables as at 31 December 2012 are as follows:

Accounting policy – Finance leases: where the Group is the lessor

Finance leases occur where the lessee has substantially all the risks and rewards of ownership of an asset.

When assets are leased out under finance leases, the present value of the lease payments is recognised as receivables. The difference between the gross receivables and the present value of the receivables is recognised as unearned finance lease interest income. Lease interest income is recognised over the term of the lease using the net investment method, which reflects a constant periodic rate of return.

| Critical accounting estimates and judgements – Classification of leases |

|---|

|

The Group classifies its leases into either finance leases or operating leases taking into account of the spirit, intention, and application of HKAS 17 "Leases". Management assesses the classification of leases by taking into account the market conditions at the inception of the lease, the period of the lease and the probability of exercising purchase options, if any, attached to the lease. For those leases that would transfer ownership of the assets to the Group at the end of the lease term, or the purchase options, if any, attached to the arrangements are sufficiently attractive as to make it reasonably certain that they would be exercised, they are being treated as finance leases. |

(b) Other receivables from disposal of RoRo

The balance related to the disposal of RoRo vessels in 2012 and represents the net purchase consideration for the two RoRo vessels that have commenced their bareboat charters to the purchaser. The non-current element of the other receivables will have been repaid by December 2015. The fair value of the other receivables is based on discounted cash flows based on a borrowing rate of 6%. The discount rate represents the Euro borrowing rate at inception including the appropriate credit spread.

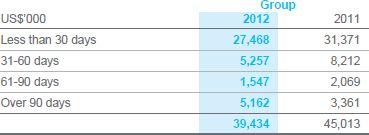

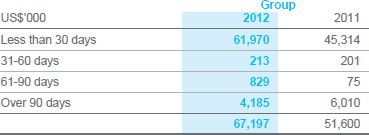

(c) Trade receivables

At 31 December 2012, the ageing of net trade receivables is as follows:

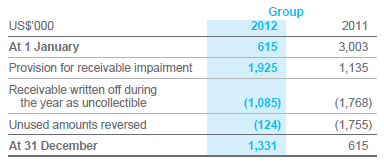

Movements in the provision for impairment of trade receivables are as follows:

Credit policy

Trade receivables consist principally of voyage-related trade receivables. It is industry practice that 95% to 100% of freight is paid upon completion of loading, with any balance paid after completion of discharge and the finalisation of port disbursements, demurrage claims or other voyage-related charges. The Group will not normally grant any credit terms to its customers.

There is no concentration of credit risk with respect to trade receivables, as the Group has a large number of international customers.

As at 31 December 2012 and 2011, net trade receivables are all past due but not impaired as no customer is expected to have significant financial difficulty. All other items within trade and other receivables do not contain past due or impaired assets.

16 CASH AND DEPOSITS

Note: The balances were held as securities with banks in relation to certain performance guarantees and as collateral for certain bank loans.

As at 31 December 2012, the Company had cash at bank of US$17,000 (2011: US$13,000).

Cash and deposits are mainly denominated in United States Dollars and the carrying values approximate their fair values due to the short-term maturities of these assets.

Accounting policy – Cash and cash equivalents

Cash and cash equivalents comprise cash on hand and deposits held with banks and other short-term highly liquid investments with original maturities of three months or less.

17 OTHER NON-CURRENT ASSETS

Other non-current assets are denominated in United States Dollars. Please refer to Note 5 for the accounting policy on impairment.

18 INVENTORIES

Accounting policy

Inventories are stated at the lower of cost and net realisable value, as estimated by the management. Costs are calculated on a first-in first-out basis.

19 STRUCTURED NOTES

Structured notes are investments under the Group Treasury Policy that are classified as financial assets at fair value through profit or loss and please refer to Note 14 for the accounting policy.

Fair value as at 31 December 2012 is measured according to the Level 3 of the fair value hierarchy defined in HKFRS 7: Financial Instruments: Disclosures. Please refer to Note 13 Fair value levels for the definitions of different levels.

Movements for the year ended 31 December 2012 are as follows:

20 TRADE AND OTHER PAYABLES

At 31 December 2012, the ageing of trade payables was as follows:

The carrying values of trade and other payables approximate their fair values due to the short-term maturities of these liabilities.

Trade and other payables are mainly denominated in United States Dollars.

Accounting policy – Trade payables

Trade payables mainly represent freight and charter-hire payables which are recognised initially at fair value and subsequently measured at amortised cost using the effective interest method.

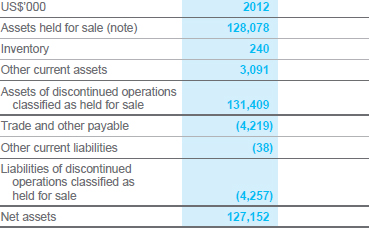

21 ASSETS AND LIABILITIES OF DISCONTINUED OPERATIONS CLASSIFIED AS HELD FOR SALE

In September 2012, the Group entered into an agreement to sell six RoRo vessels. The assets and liabilities related to the RoRo business have been presented as "held for sale". The disposal transaction will be completed when the remaining four RoRo vessels commence their bareboat charters which for three vessels occurred in February 2013 and for the remaining vessel is expected in March 2014.

(a) Assets and liabilities of discontinued operations

Note: Relates to four RoRo vessels which had not commenced their bareboat charters at 31 December 2012.

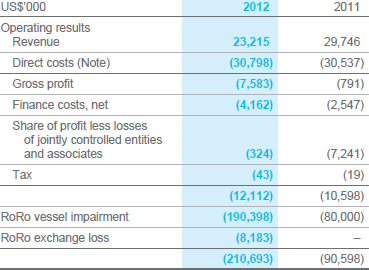

(b) Analysis of the result of the discontinued operations

Note: Includes depreciation charges for RoRo vessels of US$7,900,000 (2011: US$11,000,000).

(c) Cumulative expense recognised in other comprehensive income relating to discontinued operations

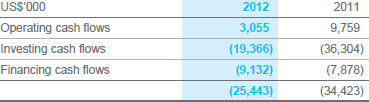

(d) The net cash flows attributable to the discontinued operations

Accounting policy – Assets and liabilities of discontinued operations classified as held for sale

Assets are classified as held for sale when their carrying amount is to be recovered principally through a sale transaction and a sale is considered highly probable. They are stated at the lower of carrying amount and fair value less costs to sell.

A discontinued operation is a component of the Group's business which represents a separate operations, or its part of a single coordinated plan to dispose of a separate major line of business or geographical area of operations, or is a subsidiary acquired exclusively with a view to resale. The operations and cash flows of a discontinued operation should be clearly distinguished from the rest of the Group.

When an operation is classified as discontinued, a single amount is presented in the income statement, which comprises the post-tax profit or loss of the discontinued operation and the post-tax gain or loss recognised on the measurement to fair value less costs to sell, or on the disposal, of the assets constituting the discontinued operation.

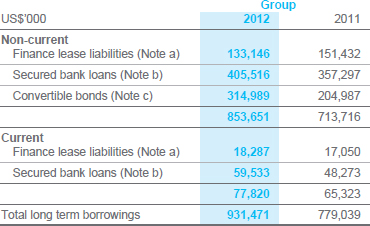

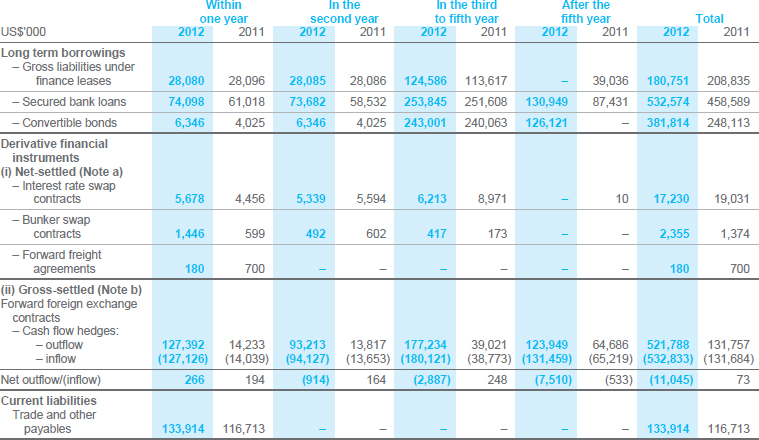

22 LONG TERM BORROWINGS

The fair value of long term borrowings is estimated by discounting the future contractual cash flows at the current market interest rate that is available to the Group for similar financial instruments.

Long term borrowings are mainly denominated in United States Dollars.

Accounting policy – Borrowings

Borrowings are recognised initially at fair value, net of transaction costs incurred. Borrowings are subsequently stated at amortised cost; any difference between the proceeds (net of transaction costs) and the redemption value is recognised in the income statement over the period of the borrowings using the effective interest method.

Borrowings are classified as current liabilities unless the Group has an unconditional right to defer settlement of the liabilities for at least twelve months after the balance sheet date.

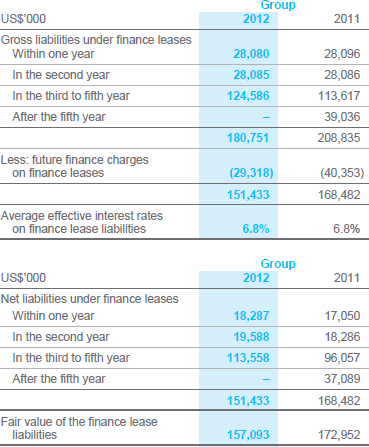

(a) Finance lease liabilities

At 31 December 2012, the Group leased certain vessels under finance leases. Under the terms of the leases, the Group has options to purchase these vessels at any time throughout the charter periods. Lease liabilities are effectively secured as the rights to the leased vessels revert to the lessors in the event of default.

The gross liabilities, future finance charges and net liabilities under finance leases as at 31 December 2012 are as follows:

Accounting policy – Finance lease: where the Group is the lessee

Leases of assets where the lessee has substantially all the risks and rewards of ownership of such assets are classified as finance leases.

Where the Group is the lessee, finance leased assets are capitalised at the commencement of the lease at the lower of the fair value of the leased assets and the present value of the minimum lease payments. Each lease payment is allocated between liability and finance charges so as to achieve a constant rate of interest on the remaining balance of the liability. The finance lease liabilities are included in current and non-current borrowings. The finance charges are expensed in the income statement over the lease periods so as to produce a constant periodic rate of interest on the remaining balance of the liability for each period. The assets accounted for as finance leases are depreciated over the shorter of their estimated useful lives or the lease periods.

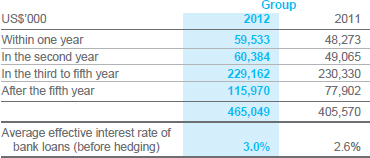

(b) Secured bank loans

The bank loans as at 31 December 2012 were secured, inter alia, by the following:

(i) Mortgages over certain owned vessels with net book values of US$695,556,000 (2011: US$548,532,000) (Note 6);

(ii) Assignment of earnings and insurances compensation in respect of the vessels;

(iii) Fixed and floating charges over all of the assets of certain subsidiaries of the Group's towage business; and

(iv) Cash and deposits totaling US$60,000,000 (2011: Nil).

The maturities of the Group's bank loans are as follows:

(c) Convertible bonds

(i) Convertible bonds – 1.75% coupon convertible bonds due 2016

| Issue size | US$230 million |

| Issue date | 12 April 2011 |

| Maturity date | 12 April 2016 (6 years from issue) |

| Coupon – cash cost | 1.75% p.a. payable semi-annually in arrears on 12 April and 12 October |

| Effective interest rate | 4.70% charged to income statement |

| Redemption Price | 100% |

| Conversion Price into shares | HK$7.26 (with effect from 24 April 2012) (Note) |

| Conversion at bondholders' options | (i) until 11 January 2014, conversion can only take place if the closing price of the Company's shares is at least at a 20% premium to the conversion price then in effect for five consecutive trading days.

(ii) After 11 January 2014 conversion can take place at any time at no premium. |

| Bondholder put date and price | On 12 April 2014 (4 years from issue), each bondholder will have the right to require the Group to redeem all or some of the bonds at 100% of the principal amount. |

| Issuer call date and price | On or after 12 April 2014, the Group may redeem the bonds in whole at a redemption price equal to 100% of their principal amount if the closing price of the Company's shares is at least at a 30% premium to the conversion price then in effect for thirty consecutive trading days. |

Note: The conversion price is subject to an adjustment arising from the cash dividends paid by the Company according to a pre-determined adjustment factor. Such adjustment becomes effective on the first date on which the Shares are traded ex-dividend.

(ii) Convertible bonds – 1.875% coupon convertible bonds due 2018

| Issue size | US$123.8 million |

| Issue date | 22 October 2012 |

| Maturity date | 22 October 2018 (6 years from issue) |

| Coupon – cash cost | 1.875% p.a. payable semi-annually in arrears on 22 April and 22 October |

| Effective interest rate | 5.17% charged to income statement |

| Redemption Price | 100% |

| Conversion Price into shares | HK$4.96 (Note) |

| Conversion at bondholders' options | Bondholders may exercise the conversion right at anytime on or after 2 December 2012. |

| Bondholder put date and price | On 22 October 2016 (4 years from issue), each bondholder will have the right to require the Group to redeem all or some of the bonds at 100% of the principal amount. |

| Issuer call date and price | On or after 22 October 2016, the Group may redeem the bonds in whole at a redemption price equal to 100% of their principal amount if the closing price of the Company's shares is at least at a 30% premium to the conversion price then in effect for thirty consecutive trading days. |

Note: The conversion price is subject to an adjustment arising from the cash dividends paid by the Company according to a pre-determined adjustment factor. Such adjustment becomes effective on the first date on which the Shares are traded ex-dividend.

Accounting policy – Convertible bonds

Convertible bonds are accounted for as the aggregate of (i) a liability component and (ii) an equity component.

At initial recognition, the fair value of the liability component of the convertible bonds is determined using a market interest rate for an equivalent non-convertible bond. The remainder of the proceeds is allocated to the conversion option as an equity component, recognised in other comprehensive income.

Transaction costs associated with issuing the convertible bonds are allocated to the liability and equity components in proportion to the allocation of proceeds. The liability component is subsequently carried at amortised cost, calculated using the effective interest method, until extinguished on conversion or maturity.

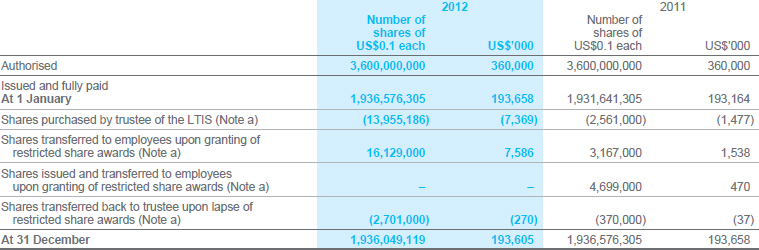

23 SHARE CAPITAL

(a) Restricted share awards

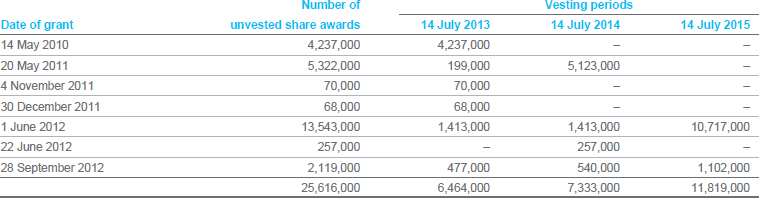

Restricted share awards under the Company's Long Term Incentive Scheme ("LTIS") were granted to Directors, senior management and certain employees. The LTIS under HKFRS is regarded as a special purpose entity of the Company. During the year, 13,753,000, 257,000 and 2,119,000 (2011: 7,886,000) restricted share awards were granted and transferred to certain employees on 1 June 2012, 22 June 2012 and 28 September 2012 respectively. The market price of the restricted share awards on the grant date represented the fair value of those shares.

The sources of the shares granted and their related movement between share capital and staff benefit reserve are as follows:

The vesting periods and grant dates of the unvested restricted share awards are as follows:

At 31 December 2012. there remained 528,000 (2011: 814) shares held by the trustee, amounting to US$52,800 (2011: US$100) as a debit to share capital.

Accounting policy

Ordinary shares are classified as equity. Incremental costs directly attributable to the issue of new shares or options are shown in equity as a deduction from the proceeds.

Where any group company purchases the Company's equity share capital, the consideration paid, including any directly attributable incremental costs (net of income taxes), is deducted from equity until the shares are cancelled, reissued or disposed of. Where such shares are subsequently sold or reissued, any consideration received (net of any directly attributable incremental transaction costs and the related income tax) is included in equity.

(b) Share options

55,500,000 share options under the LTIS were granted to Directors, senior management and certain employees on 14 July 2004 at an exercise price of HK$2.5 per share. They were fully vested on 14 July 2007 and will expire on 14 July 2014. At 31 December 2012, all of the 400,000 (2011: 400,000) outstanding share options were exercisable and their average exercise price was HK$2.50. There was no movement in the number of share options outstanding during the period.

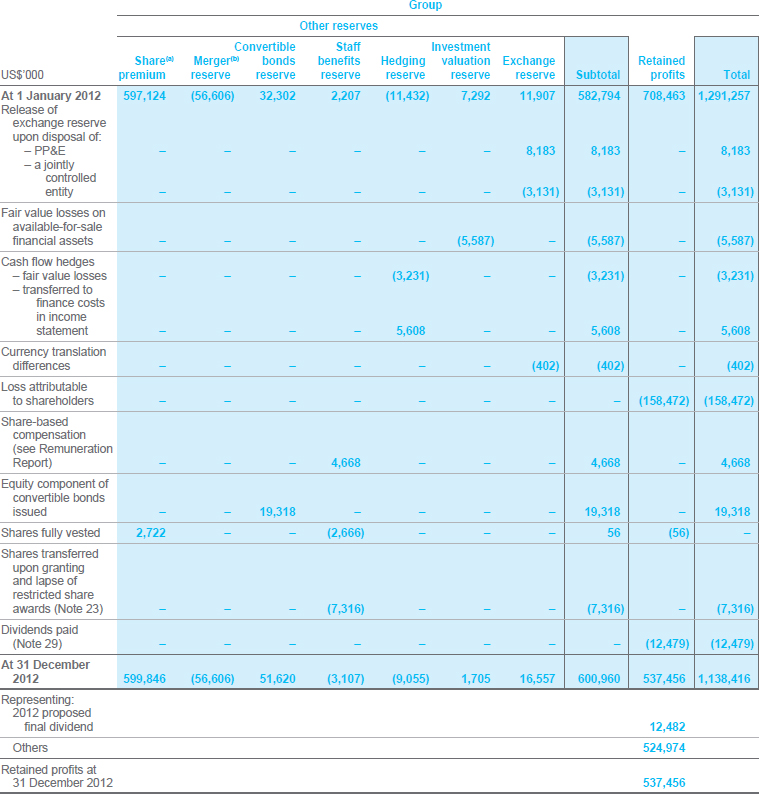

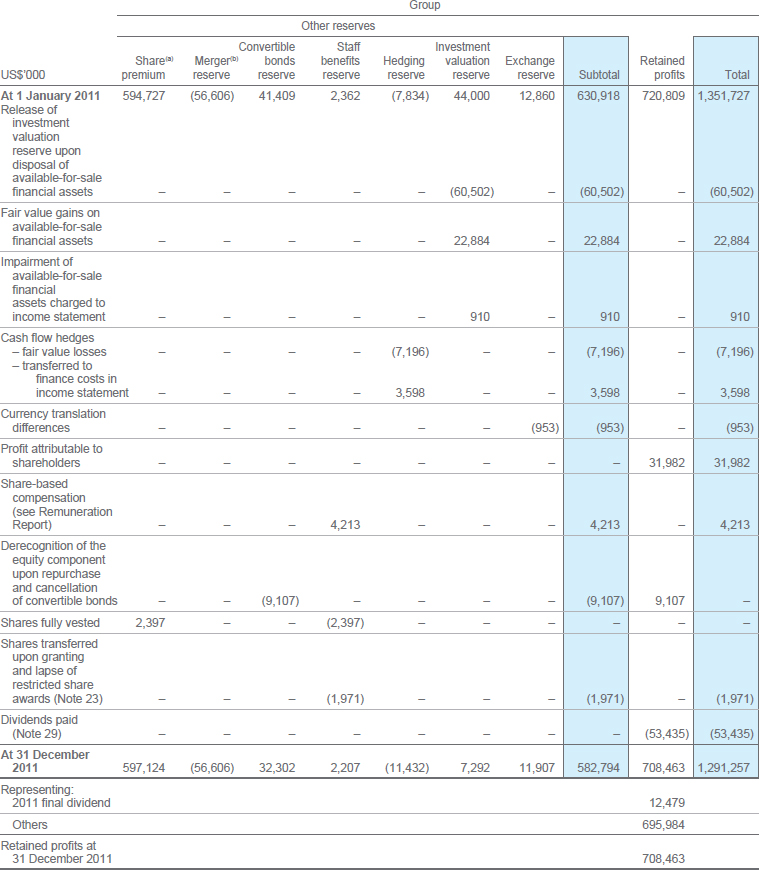

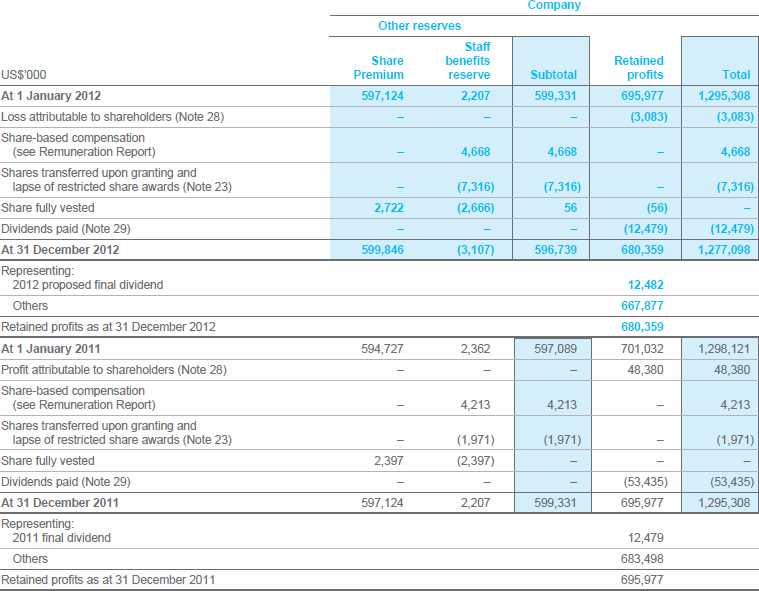

24 RESERVES

(a) Share premium mainly represents the net issuance proceeds in excess of the nominal value of shares issued credited to share capital.

(b) Merger reserve of the Group represents the difference between the nominal value of the shares of subsidiaries acquired and the nominal value of the Company's shares issued pursuant to the transfer of PB Vessels Holding Limited and its subsidiaries into the Company through an exchange of shares prior to the listing of the shares of the Company on the Stock Exchange in 2004.

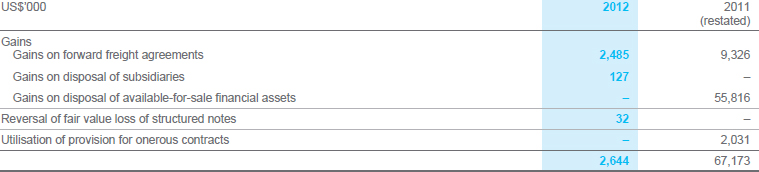

25 OTHER INCOME AND GAINS

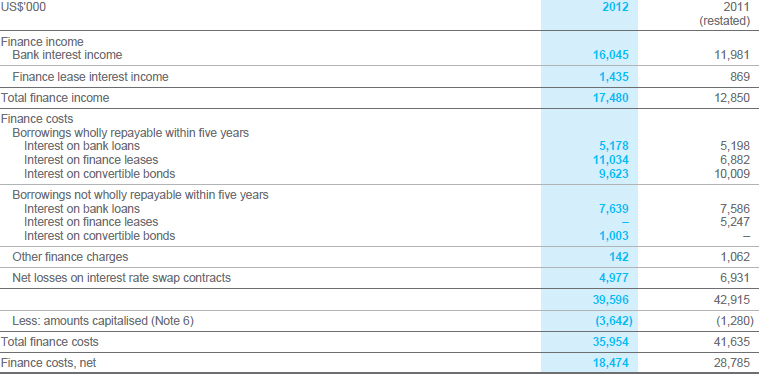

26 FINANCE INCOME AND COSTS

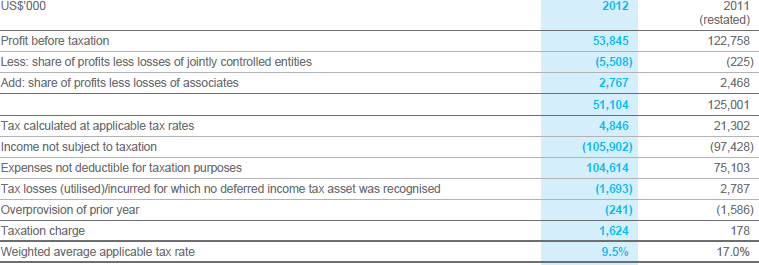

27 TAXATION

Shipping income from international trade is either not subject to or exempt from taxation according to the tax regulations prevailing in the countries in which the Group operates. Shipping income from towage and non-shipping income is subject to tax at prevailing rates in the countries in which these businesses operate.

The amount of taxation charged/(credited) to the consolidated income statement represents:

The tax on the Group's profit before taxation differs from the theoretical amount that would arise using the applicable tax rate, being the weighted average of rates prevailing in the countries in which the Group operates, as follows:

The Group has not recognised deferred income tax assets of US$8,581,000 (2011: US$10,274,000) in respect of tax losses amounting to US$28,604,000 (2011: US$36,735,000). These tax losses have no expiry date.

| Critical accounting estimates and judgements – Income taxes |

|---|

|

The Group is subject to income taxes in certain jurisdictions. There are transactions entered into where the ultimate tax determination and tax classification may be uncertain. Significant judgement is required in determining the provision for income taxes. The current provision in the balance sheet for income tax of US$2,509,000 represents management's estimates of the most likely amount of tax expected to be paid to the taxation authorities. Where the final tax outcome of these matters is different from the amounts that were initially recorded, such differences will impact the provision for income tax in the period in which such determination is made. |

Accounting policy – Current income tax

The current income tax charge is calculated on the basis of the tax laws enacted or substantively enacted at the balance sheet date in the countries where the Company and its subsidiaries, jointly controlled entities and associates operate and generate taxable income. Management periodically evaluates positions taken in tax returns with respect to situations in which applicable tax regulations is subject to interpretation and establishes provisions where appropriate on the basis of amounts expected to be paid to the tax authorities.

Accounting policy – Deferred income tax

Deferred income tax is provided in full, using the liability method, on temporary differences arising between the tax bases of assets and liabilities and their carrying amounts in the financial statements. However, the deferred income tax is not accounted for if it arises from initial recognition of an asset or liability in a transaction other than a business combination that at the time of the transaction affects neither accounting nor taxable profit or loss. Deferred income tax is determined using tax rates (and laws) that have been enacted or substantially enacted by the balance sheet date and are expected to apply when the related deferred income tax asset is realised or the deferred income tax liability is settled.

Deferred income tax assets are recognised to the extent that it is probable that future taxable profit will be available against which the temporary differences can be utilised.

Deferred income tax is provided on temporary differences arising on investments in subsidiaries, jointly controlled entities and associates, except where the timing of the reversal of the temporary difference is controlled by the Group and it is probable that the temporary difference will not reverse in the foreseeable future.

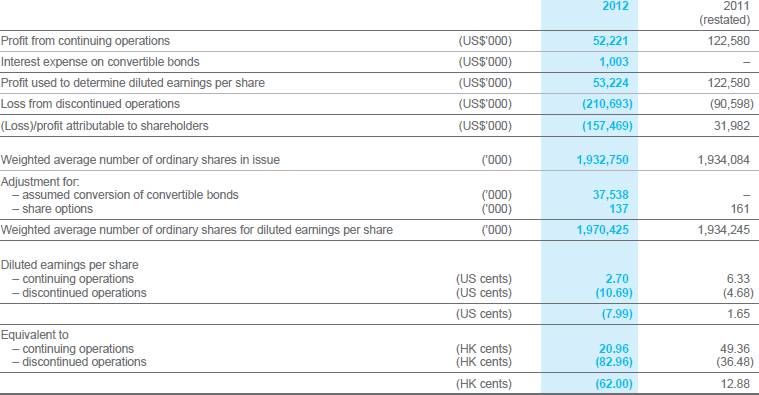

28 LOSS/PROFIT ATTRIBUTABLE TO SHAREHOLDERS

US$3,083,000 of loss (2011: US$48,380,000 of profit) attributable to shareholders is dealt with in the financial statements of the Company.

29 DIVIDENDS

The proposed final dividend is subject to the approval of the shareholders at the Annual General Meeting on 19 April 2013.

Accounting policy

Dividend distributions to the Company's shareholders are recognised as liabilities in the Group's financial statements in the period in which the dividends are approved by the Company's shareholders or Directors, where appropriate.

The dividend declared after the year end is not reflected as a dividend payable in the financial statements of that year, but will be reflected as an appropriation of retained profits for the following year.

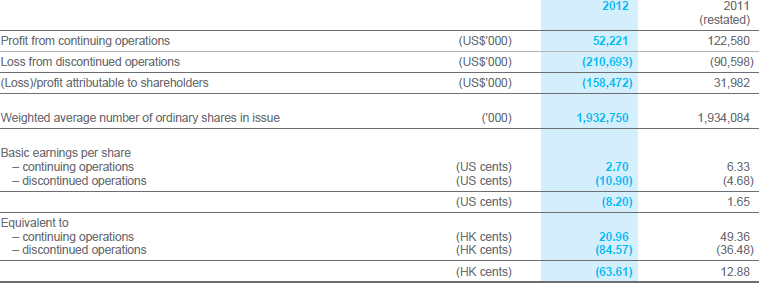

30 EARNINGS PER SHARE

(a) Basic earnings per share

Basic earnings per share are calculated by dividing the Group's profit attributable to shareholders by the weighted average number of ordinary shares in issue during the year, excluding the shares held by the trustee of the Company's LTIS (Note 23(a)).

(b) Diluted earnings per share

Diluted earnings per share are calculated by dividing the Group's profit attributable to shareholders by the weighted average number of ordinary shares in issue during the year after adjusting for the number of potential dilutive ordinary shares granted under the Company's LTIS but excluding the shares held by the trustee of the Company's LTIS (Note 23(a)).

31 NOTES TO THE CONSOLIDATED CASH FLOW STATEMENT

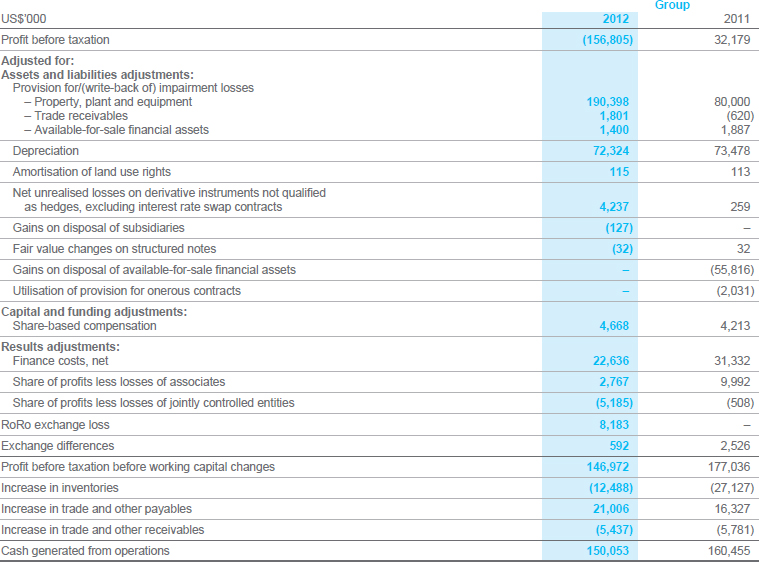

Reconciliation of profit before taxation to cash generated from operations

32 COMMITMENTS

(a) Capital commitments

Capital commitments for the Group that fall due in one year or less amounted to US$215.0 million (2011: US$181.2 million).

As at 31 December 2012 and 2011, the Company had no capital commitments.

(b) Commitments under operating leases

Accounting policy – Operating leases

Leases in which a significant portion of the risks and rewards of ownership are retained by the lessor are classified as operating leases.

| Critical accounting estimates and judgements – Classification of leases |

|---|

|

The Group classifies its leases into either finance leases or operating leases taking into account of the spirit, intention, and application of HKAS 17 "Leases". Management assesses the classification of leases by taking into account the market conditions at the inception of the lease, the period of the lease and the probability of exercising purchase options, if any, attached to the lease. For those leases that would not transfer ownership of the assets to the Group at the end of the lease term, and that it is not reasonably certain that the purchase options, if any, attached to the arrangements would be exercised, they are being treated as operating leases. |

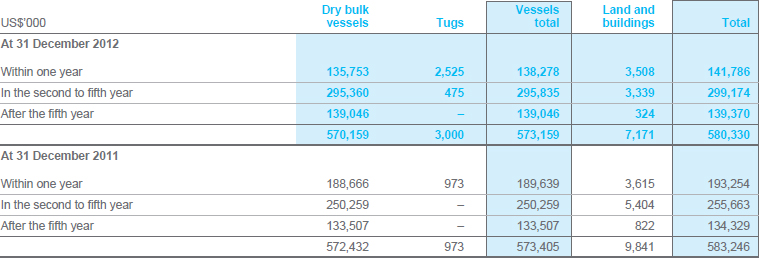

(i) The Group as the lessee – payments

The Group had future aggregate minimum lease payments under non-cancellable operating leases as follows:

Contingent lease payments made amounted to US$57,065,000 (2011: US$44,150,000). These relate to chartered-in dry bulk vessels on an index-linked basis.

The leases have varying terms ranging from less than 1 year to 11 years. Certain of these leases have escalation clauses, renewal rights and purchase options.

Accounting policy – Operating leases: where the Group is the lessee

Payments made under operating leases (net of any incentives received from the lessor) are charged to the income statement on a straight-line basis over the lease periods.

(ii) The Group as the lessor – receipts

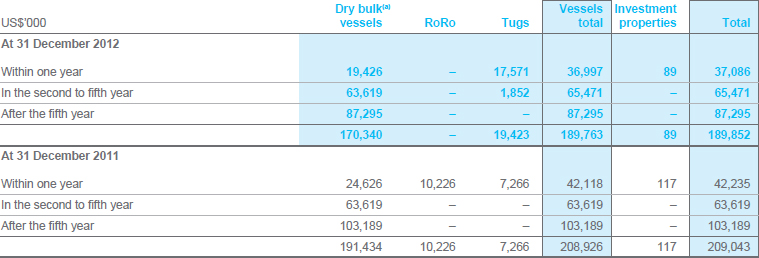

The Group had future aggregate minimum lease receipts under non-cancellable operating leases as follows:

(a) Operating lease commitments of the Group as the lessor for dry bulk vessels mainly included the commitments from two Post-Panamax vessels of US$166.8 million (2011:US$182.7 million).

The Group's operating leases are for terms ranging from less than 1 year to 16 years.

Accounting policy – Operating leases: where the Group is the lessor

When the Group leases out assets under operating leases, the assets are included in the balance sheet and, where applicable, are depreciated in accordance with the Group's depreciation policies as set out in Note 6 Property, plant and equipment. Revenue arising from assets leased out under operating leases is recognised on a straight-line basis over the lease periods.

33 FINANCIAL LIABILITIES SUMMARY

Maturity profile of the Group's financial liabilities, net-settled derivative financial instruments and gross-settled derivative financial instruments, representing contractual cash flows which include principal and interest elements where applicable, based on the remaining period from the balance sheet date to the contractual maturity date.

(a) Net-settled derivative financial instruments represent derivative liabilities whose terms result in settlement by a netting mechanism, such as settling the difference between the contract price and the market price of the financial liabilities.

(b) Gross-settled derivative financial instruments represent derivative assets or liabilities which are not settled by the above mentioned netting mechanism.

34 SIGNIFICANT RELATED PARTY TRANSACTIONS

Significant related party transactions carried out in the normal course of the Group's business and on an arm's length basis were as follows:

(a) Purchases of services

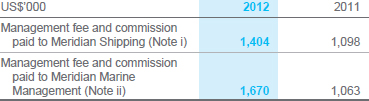

(i) The Group paid to Meridian Shipping, a jointly controlled entity, management fees and commissions in relation to commercial management services.

(ii) The Group paid to Meridian Marine Management, a jointly controlled entity, management fees and commissions in relation to technical management services.

(b) Sales of services

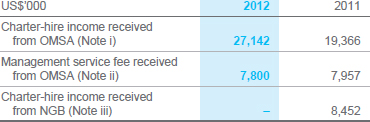

(i) The Group leased out certain vessels to OMSA, a jointly controlled entity.

(ii) The Group performed technical and other management services to OMSA.

(iii) The Group leased out certain vessels to NGB, an associate.

(c) Key management compensation

please refer the Remuneration Report.

35 FINANCIAL GUARANTEES