|

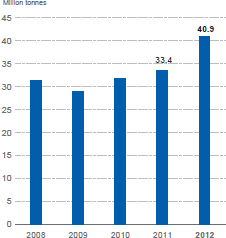

Pacific Basin Cargo Volumes 2008 - 2012  |

Our dry bulk business has been primarily focused on two key objectives for 2012: i) to grow our dry bulk fleet through inward charters and secondhand purchases of high-quality ships at attractive rates and price; and ii) to grow our customer and cargo contract portfolio globally to manage our market exposure.

Our fleet investment, composition & deployment

- Backed by customer demand, we expanded our operated fleet to an average of 155 dry bulk ships in 2012 - up from 131 in 2011 - cementing our position as the world's largest operator of high-quality Handysize tonnage with a significant Handymax presence.

- This expansion was primarily due to more chartered-in ships, including several on market-index-linked leases which align our cost base to the market while increasing our fleet scale and the synergies from better ship and cargo combinations. A larger fleet of interchangeable ships enables us to further improve customer satisfaction by increasing our flexibility in voyage timing and frequency as well as our scheduling reliability through ship substitutions in case of delays.

- A better performance in the second half of 2012 was due to a stronger third quarter and partly attributable to improved Handymax results when inward charters were renewed or replaced at lower rates in line with the weak market, gradually reducing the cost of our chartered fleet.

- We returned to the ship acquisitions market in September 2012, at which time vessel prices had softened by about 30% compared to the beginning of the year. Initially focused on secondhand ships, we have acquired six Handysize vessels and one Handymax vessel, of which one joined our fleet in fourth quarter 2012 and the balance are scheduled to join in first half 2013. We have also acquired one Handysize newbuilding resale which is due to deliver in May.

- We have also entered into agreements to long-term charter several Handysize ships for periods up to seven years.

- We now await the delivery of 16 owned and five chartered ships (including 17 newbuildings) in 2013 to 2015.

- Our two newest chartering offices in Beijing and Durban have now been operational for over a year and have generated new customers, new long-term cargo contracts and new parcelling and project cargo business to supplement our traditional bulk-based activity. Our network of 10 commercial dry bulk offices across six continents allows us to develop and nurture strong customer relationships, and to develop additional cargo opportunities to complement the planned growth of our fleet.

Investing in our people

- We formalised our dry bulk trainee programme in 2012, and three recruitment intakes in recent months will serve to prepare seven talented young individuals for postings in our Hong Kong, Stamford, Santiago, Melbourne, Auckland and London offices to enhance our strong talent pool in Pacific Basin Dry Bulk.

OPPORTUNITIES

OPPORTUNITIES

- China's continued strong demand for minor bulk commodities

- Global trade imbalances and fleet utilisation inefficiencies stemming from China's dominant share of global bulk imports

- Stronger than anticipated US economic recovery and revived industrialisation in North America

- Fewer newbuilding deliveries as shipyards slow production to stretch out their orderbooks

- Continued high levels of scrapping of dry bulk capacity

- Bank lending constraints limit funding for ship acquisitions, raising barriers to entry and increasing opportunities for shipowners with available cash

THREATS

THREATS

- Still excessive albeit reduced overhang of dry bulk vessel supply and excessive shipbuilding capacity

- Global economic recovery negatively impacted by further shocks relating to European finances and US government spending

- Premature shipowner optimism resulting in less scrapping, increased ordering activity and increased vessel prices

- Increased national protectionism impacting raw materials trade

- Potentially weaker growth in Chinese minor bulk imports depending on extent of economic and industrial slow down

We expect the dry bulk market to remain weak overall in 2013 with seasonal variations prompting annual lows in the first quarter followed by modest recovery in the second.

Despite continued global economic weakness, dry cargo demand is likely to be similarly healthy as last year.

Supply-side fundamentals are improving, especially in the Handysize segment where we expect substantially no net fleet growth this year. However it will take some time for the market to absorb the over-supply of larger dry bulk ships generated by the newbuilding boom in recent years, and before a sustained recovery becomes apparent.

Conditions overall are likely to remain challenging, thereby generating further vessel acquisition opportunities for shipowners with available cash. However, premature shipowner optimism may result in increased vessel prices thus impacting the availability of attractively priced ships and undermining our key strategic objective for the year.

We remain optimistic about the longer term. We expect high levels of ship scrapping and limited new ship ordering to moderate dry bulk ship supply expansion while demand remains relatively robust as emerging economies continue to industrialise and grow.

STRATEGY

As a highest priority, we will seek further opportunities to invest in high-quality Handysize and Handymax ships to expand our owned fleet.

We aim also to expand our dry bulk customer and cargo portfolio in tandem with our core fleet expansion.

Our exposure to the weak freight market will be partly limited by our cargo book which currently provides cover for 55% of our Handysize revenue days in 2013.

We are working on initiatives to further improve our customer service, such as through decentralised operational support and increased customer engagement at a local level to ensure best-in-class service, and to take us a step closer to our industry leadership vision.

We continue to draw on our customer-focused business model, the scale and flexibility of our fleet, our drive for efficiency and our strong balance sheet to ensure we are best positioned to maximise our performance in the current challenging conditions and to capitalise on opportunities and eventual improvements in market conditions.