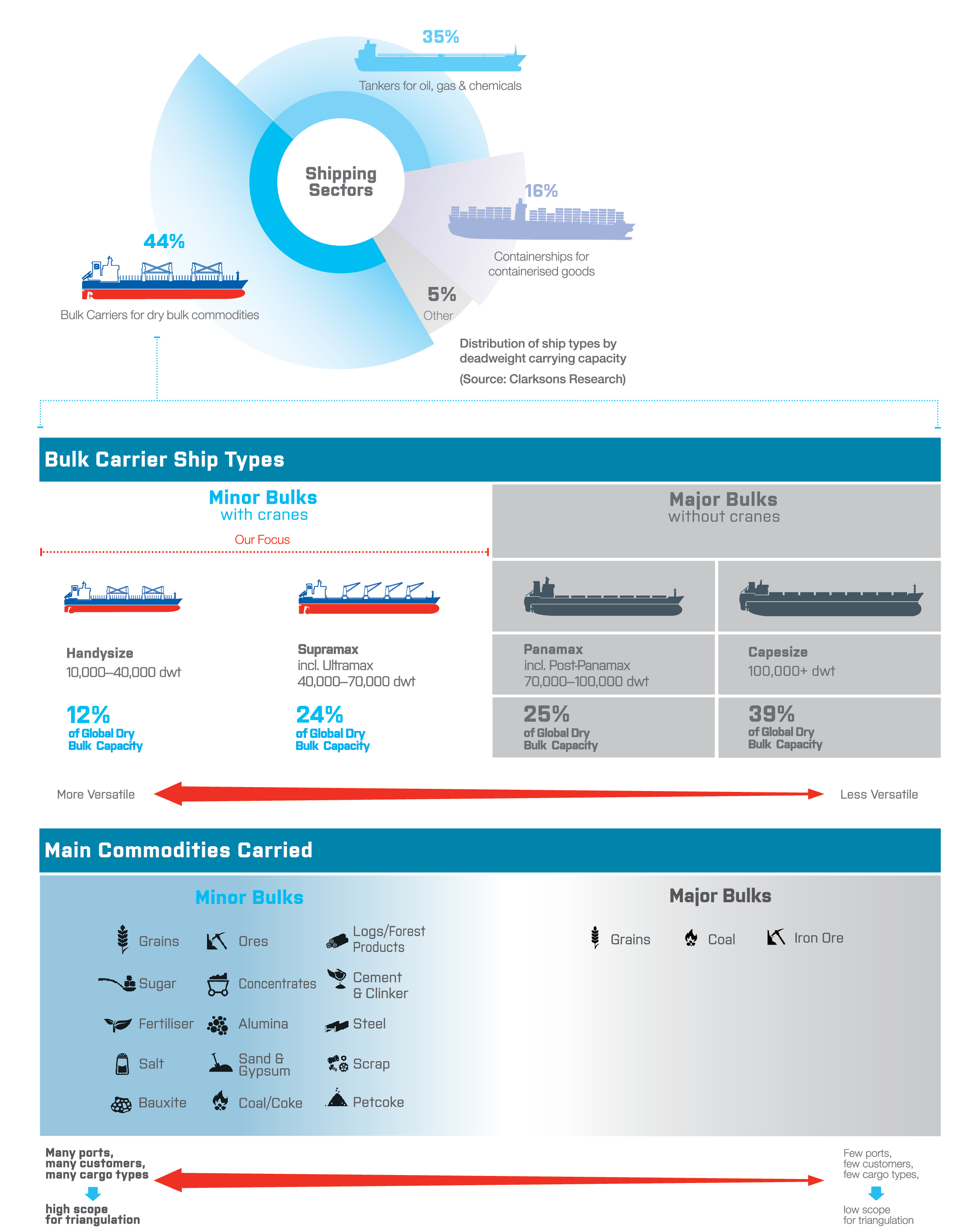

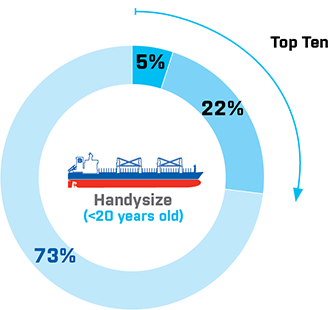

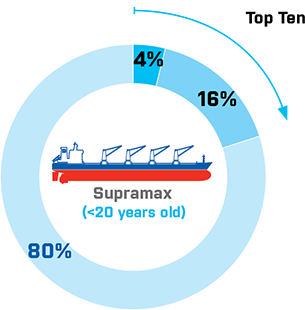

We are one of the world's largest Handysize and Supramax owners and operators in a highly fragmented market that revolves around the carriage of minor bulks.

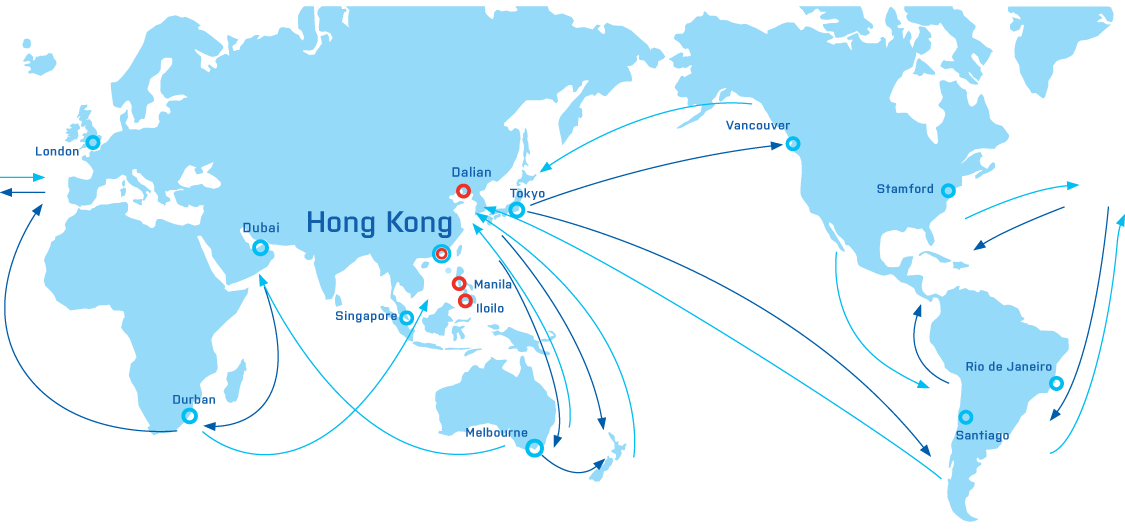

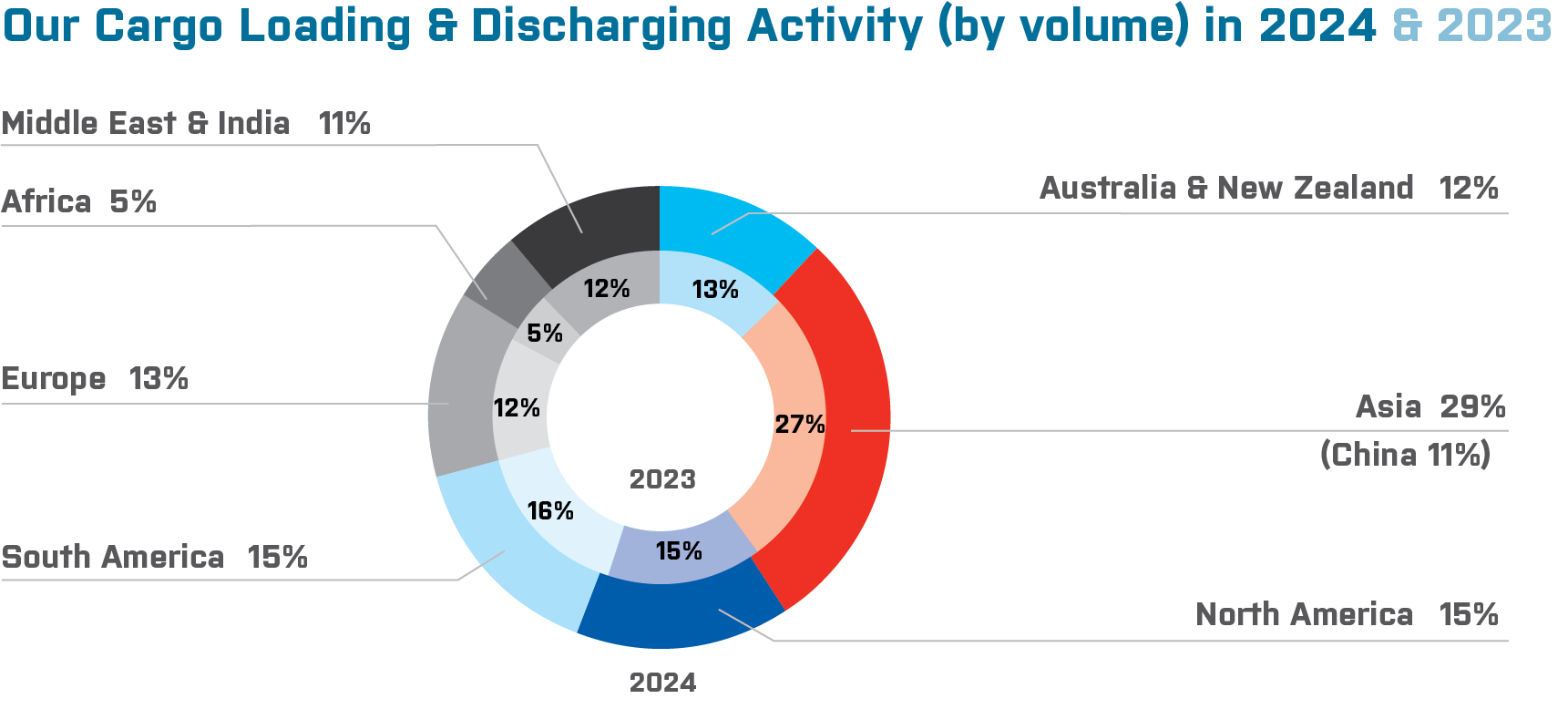

Minor bulk commodities are very varied, controlled by a large number of customers and transported via a large number of ports globally, enabling triangular trading and thus high vessel utilisation. This segment requires versatile self-loading and discharging (“geared”) ships of “handy” proportions to allow them access to the many ports around the world restricted by shallow water, locks, narrow channels and river bends.

By contrast, cargo demand for large bulk carriers comprises only a few major bulk commodities controlled by a handful of cargo owners and transported through a much smaller number of ports, making them heavily dependent on relatively few trades and hence their prospects are more volatile. Their activity is typically characterised by one-way laden transportation resulting in lower utilisation.

We are focused on a particular ship segment and size, but are diversified geographically and in terms of customers and cargoes. This allows us scope to triangulate our voyages – such as by combining fronthaul and backhaul trades – and thus enhance our vessel utilisation and earnings. We do not participate in the volatile freight earnings that large bulk carriers can achieve, but we are well positioned to achieve our important aim of generating a steadier and more sustainable earnings stream with better protected earnings in the down-cycle through our business model.

Our earnings reliability is further enhanced by the fact that global Handysize capacity has experienced only relatively modest growth in the past decade compared to the much larger expansion of the major bulk fleets.